ABOUT AUTHOR

Youness EL Kandoussi is a seasoned Consultant Risk Expert with over 23 years of experience in Operational Risk Management, Islamic Finance, and Professional Training. He holds a certification as an Operational Risk Expert from the London School of Business & Finance (2018). Throughout his career, Youness has successfully led numerous large-scale projects for various banks, from conception to completion, ensuring their success in terms of costs and timelines. He has also been actively involved in conducting training programs on Risk Management for executives and employees of Financial Institutions, Public Administrations, Cooperatives, and Associations. Accomplishments Youness EL Kandoussi's notable accomplishments include: • Conducting successful certified training programs in Risk Management for professionals across different sectors. • Moderating and participating in various seminars and conferences within the financial industry and FinTech. • Implementing Operational Risk Management Systems and Risk Mapping for prominent institutions like SGMA, CDG Invest, and Umnia Bank. • Leading the implementation of Operational Risk Management Systems and Reporting projects, including functional specifications development and System implementation.

READ ALSO

Context In the last few days, several businesses, including aviation and banking sectors, experienced significant disruptions due to issues with Microsoft services. This outage affected various cloud-based services, including Microsoft 365, Azure, and Teams. The interruptions were caused by a combination of network configuration changes and infrastructure issues within Microsoft's global network (https://www.reedsmith.com/en/perspectives/2024/02/business-interruption-claims-in-2024-a-global-perspective) (https://status.cloud.microsoft/#:~:text=URL%3A%20https%3A%2F%2Fstatus,100). The outage highlighted the increasing reliance of global industries on cloud services and the significant impact such disruptions can have on business operations, from communication breakdowns to halted transactions (https://www.businesswire.com/news/home/20240116375142/en/Allianz-Risk-Barometer-A-Cyber-Event-Is-the-Top-Global-Business-Risk-for-2024). While Microsoft worked to resolve the issues, it underscored the importance of robust cyber risk management and contingency planning in mitigating the effects of such outages (https://www.nortonrosefulbright.com/en/knowledge/publications/20530078/the-cyber-risks-faced-by-the-aviation-industry---ten-things-to-know). The recent Microsoft outages, which disrupted services like Microsoft 365, Teams, and Outlook, were primarily caused by a series of technical and security issues. Initially, Microsoft identified that a "wide-area networking (WAN) routing change" led to connectivity problems. This change triggered issues with network latency and timeouts, affecting how packets were forwarded across Microsoft's global network. This impacted users' ability to access various cloud services, including Azure, SharePoint, and OneDrive (https://www.bankinfosecurity.com/microsoft-365-cloud-service-outage-disrupts-users-worldwide-a-21017) (https://www.techradar.com/news/this-is-what-caused-the-recent-huge-microsoft-365-and-teams-outage). Additionally, Microsoft faced cyber risks, particularly distributed denial-of-service (DDoS) attacks. These attacks, launched by a group known as Storm-1359, aimed to disrupt services by overwhelming Microsoft's infrastructure with malicious traffic. The DDoS attacks targeted layer 7 of the OSI model, affecting HTTP(S) traffic and causing resource exhaustion and slowdowns (https://msrc.microsoft.com/blog/2023/06/microsoft-response-to-layer-7-distributed-denial-of-service-ddos-attacks/). To mitigate these issues, Microsoft rolled back the problematic network changes and implemented additional protections to prevent similar disruptions in the future. These measures included enhancing their Web Application Firewall (WAF) and adding stricter controls on network command executions to avoid unintended consequences from network changes (https://www.bankinfosecurity.com/microsoft-experiences-second-major-cloud-outage-in-2-weeks-a-21134) (https://www.techradar.com/news/this-is-what-caused-the-recent-huge-microsoft-365-and-teams-outage). In recent days, significant disruptions in Microsoft services have caused major headaches for businesses worldwide. Industries ranging from aviation to banking found themselves grappling with unexpected downtime, impacting critical operations and highlighting a growing reliance on cloud-based services. This article explores whether Microsoft should be held legally accountable for failing to ensure business continuity for its global customers. The Outage and Its Impacts The recent Microsoft outages affected a range of cloud services, including Microsoft 365, Azure, and Teams. These disruptions were triggered by a combination of network configuration changes and infrastructure issues within Microsoft’s global network. Specifically, a "wide-area networking (WAN) routing change" led to severe connectivity problems. This change caused network latency and timeouts, disrupting the forwarding of data packets across Microsoft's global network. As a result, users experienced significant issues accessing cloud services such as Azure, SharePoint, and OneDrive. In addition to technical glitches, Microsoft also faced cyber threats, particularly distributed denial-of-service (DDoS) attacks. A group known as Storm-1359 targeted Microsoft’s infrastructure with malicious traffic, aiming to exhaust resources and slow down services. These attacks impacted layer 7 of the OSI model, affecting HTTP(S) traffic and causing further disruptions. The Importance of Business Continuity These outages underscore the critical role that cloud services play in modern business operations. From communication breakdowns to halted transactions, the ripple effects of such disruptions can be severe. The aviation and banking sectors, in particular, experienced significant operational impacts, illustrating the high stakes involved. As businesses increasingly rely on cloud services for their day-to-day operations, the importance of robust cyber risk management and contingency planning becomes more apparent. Legal and Ethical Considerations Given the scale and impact of these disruptions, the question arises: should Microsoft be sued for not ensuring business continuity? On one hand, businesses rely on service level agreements (SLAs) with cloud providers like Microsoft to guarantee a certain level of uptime and reliability. When these expectations are not met, it can lead to substantial financial losses and operational challenges. Businesses may argue that Microsoft failed to uphold its end of the agreement, warranting legal action to recover damages. On the other hand, the complexity of managing a global cloud infrastructure means that occasional outages are inevitable. Microsoft did take immediate steps to mitigate the issues, rolling back problematic network changes and enhancing protections against future disruptions. These efforts demonstrate a commitment to resolving the issues and improving service reliability. Cyber Risk Management and Contingency Planning The outages highlight the need for businesses to adopt comprehensive cyber risk management strategies and contingency plans. Relying solely on a single cloud provider can expose businesses to significant risks. Diversifying cloud services and implementing robust backup systems can help mitigate the impact of such outages. Additionally, regular testing and updating of contingency plans can ensure that businesses are better prepared to handle unexpected disruptions. Conclusion While the recent Microsoft outages have caused significant disruptions, suing the tech giant may not be the most effective solution. Instead, businesses should focus on enhancing their own cyber risk management and contingency planning efforts. By diversifying cloud services and implementing robust backup systems, businesses can better protect themselves against future outages. At the same time, cloud providers like Microsoft must continue to improve their infrastructure and security measures to minimize the risk of such disruptions and maintain customer trust. The recent events serve as a stark reminder of the interconnected nature of modern business operations and the importance of resilience in the face of unexpected challenges. References https://www.reedsmith.com/en/perspectives/2024/02/business-interruption-claims-in-2024-a-global-perspective https://status.cloud.microsoft/#:~:text=URL%3A%20https%3A%2F%2Fstatus,100). (https://www.businesswire.com/news/home/20240116375142/en/Allianz-Risk-Barometer-A-Cyber-Event-Is-the-Top-Global-Business-Risk-for-2024 https://www.nortonrosefulbright.com/en/knowledge/publications/20530078/the-cyber-risks-faced-by-the-aviation-industry---ten-things-to-know https://www.bankinfosecurity.com/microsoft-365-cloud-service-outage-disrupts-users-worldwide-a-21017 https://www.techradar.com/news/this-is-what-caused-the-recent-huge-microsoft-365-and-teams-outage https://msrc.microsoft.com/blog/2023/06/microsoft-response-to-layer-7-distributed-denial-of-service-ddos-attacks/

by Youness El Kandoussi | 2 years ago | 0 Comment(s) | 1121 Share(s) | Tags :

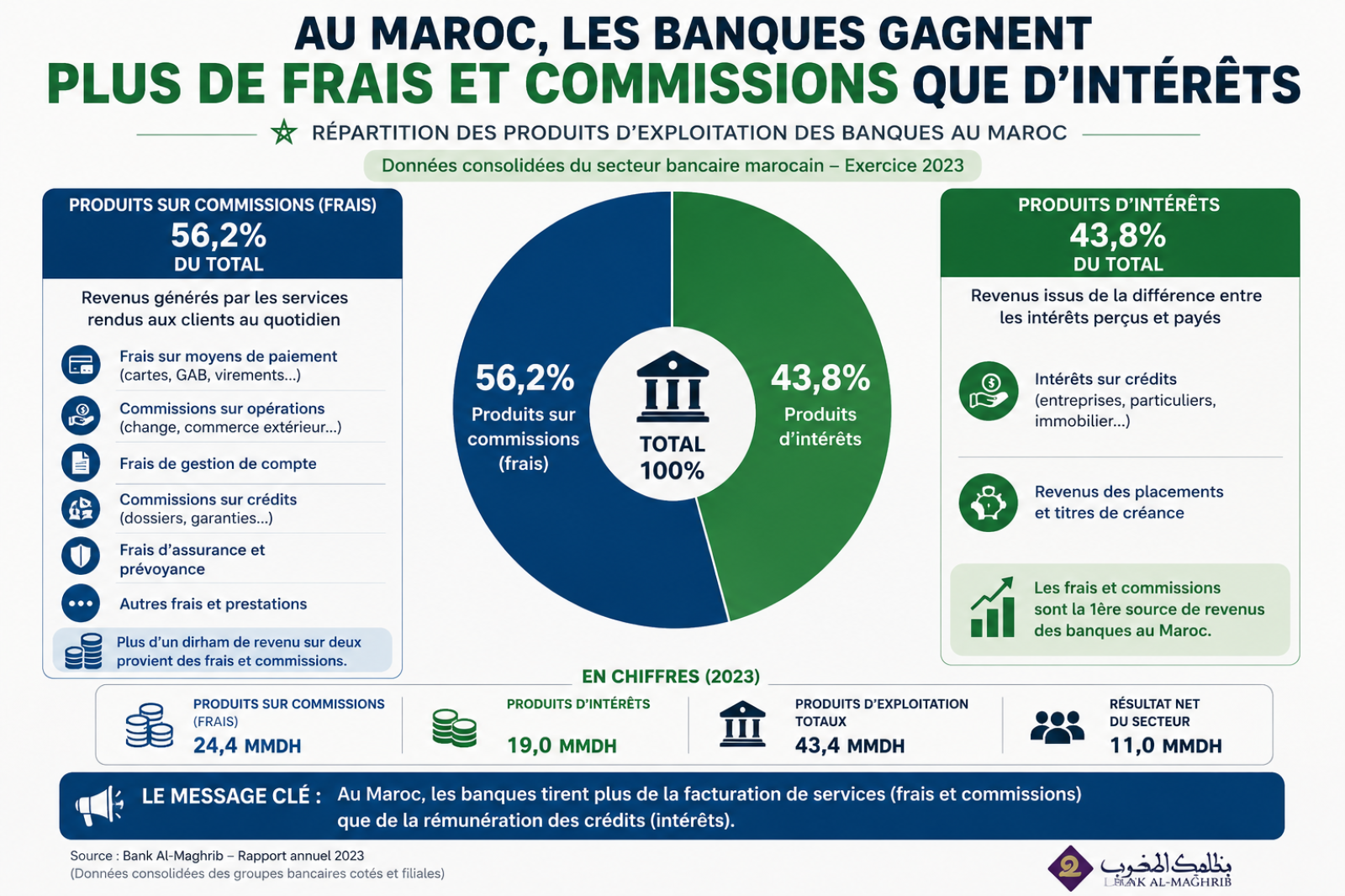

CONTEXTE ET CADRE DE L'ANALYSE Le modèle de revenus des banques commerciales repose sur deux piliers structurels : le revenu net d'int rêts (NII) — diff rentiel entre taux prêteurs et d posants — et les revenus hors int rêts (Non-Interest Revenue, NIR), qui agrègent commissions, frais de services, gains sur change, revenus de trading et autres charges factur es à la clientèle. Cette analyse porte exclusivement sur le second pilier. Dans les march s mergents d'Afrique et du Moyen-Orient, les frais et commissions bancaires constituent à la fois un levier de rentabilit pour les tablissements et un facteur de friction pour l'accès aux services financiers des m nages. Le Maroc, en tant qu' conomie mergente de r f rence en Afrique du Nord et sub-saharienne, offre un terrain d'analyse particulièrement pertinent. 1.1 P rimètre de comparaison L'analyse retient comme pays comparables ceux pr sentant des similarit s structurelles avec le Maroc selon les critères suivants : Revenu interm diaire inf rieur ou sup rieur (classification Banque Mondiale) Taux de bancarisation inf rieur à 80 % (march s d'inclusion en cours) Pr sence d'un secteur bancaire r gul et d'une banque centrale op rationnelle Proximit g ographique ou d'int gration r gionale : Afrique du Nord, Afrique subsaharienne francophone, Proche-Orient mergent Les pays retenus sont : Tunisie, Égypte, S n gal, Côte d'Ivoire, Kenya, Jordanie et, pour r f rence r gionale haute, l'Afrique du Sud. 1.2 M thodologie et sources Les donn es mobilis es proviennent des sources institutionnelles suivantes, toutes accessibles via les liens actifs de la section R f rences en fin de document : Banque Mondiale — Global Financial Development Database (GFDD/FRED) : indicateur GFDD.EI.03 (Non-Interest Income / Total Income) Bank Al-Maghrib (BAM) — Rapports annuels sur les statistiques bancaires 2023–2024 FMI — Article IV Consultation Maroc 2024 McKinsey Global Institute — « From Potential to Performance: African Banking » (mars 2026) Banque Centrale de Tunisie (BCT), BCEAO, donn es sectorielles publi es Grilles tarifaires officielles GPBM / banques marocaines (2025) STRUCTURE DES FRAIS BANCAIRES AU MAROC 2.1 Un socle de gratuit r glement e depuis 2006 Depuis l'accord de 2006 entre le Groupement Professionnel des Banques du Maroc (GPBM) et Bank Al-Maghrib, un socle minimal de services est fourni gratuitement à la clientèle : ouverture et clôture de compte, d livrance de ch quier, envoi mensuel de relev s, versements d'espèces au guichet. Cette d cision a constitu un premier levier d'inclusion, mais son p rimètre reste limit face à l' tendue r elle des charges factur es. 2.2 Grille tarifaire — Principales cat gories (2025) Cat gorie de frais Fourchette (MAD) R gime r glementaire Tenue de compte (particulier) 180 – 300 MAD/an Encadr GPBM/BAM Carte bancaire Visa Classic 120 – 180 MAD/an Tarification libre Virement hors place (agence) 15 – 40 MAD/op r. Non plafonn Virement via digital Gratuit – 10 MAD Encourag (SNIF) Opposition sur chèque 150 – 200 MAD Non plafonn Attestation / Certificat bancaire 50 – 100 MAD Non plafonn Commission de change (devises) 1 – 3 % du montant Encadr BAM Commission paiement lectronique 0,65 % transaction Plafonn BAM 2024 Retrait interbancaire (autre r seau) 5 – 15 MAD/op r. Encadr CMI → ouvert 2025 Frais de rejet (chèque sans provision) 200 – 400 MAD Barème l gal Ouverture de compte Gratuit Accord GPBM 2006 Clôture de compte Gratuit Accord GPBM 2006 Source : Grilles tarifaires GPBM, Attijariwafa Bank, Banque Populaire, CIH, BMCE — 2025. 2.3 Évolution de la part NIR/Total revenus (World Bank GFDD.EI.03) Ann e 2017 2018 2019 2020 2021 NIR / Total revenus 38,4 % 36,9 % 39,9 % 38,4 % 40,3 % Source : World Bank Global Financial Development Database — FRED Series DDEI03MAA156NWDB. ◆ Lecture analytique : Une part NIR de 40 % signifie que, pour 100 MAD de revenu bancaire total, 40 MAD proviennent de frais, commissions et activit s hors cr dit. Ce ratio — stable et lev — traduit une d pendance structurelle au modèle de facturation de services, ind pendamment du cycle de taux directeurs. III. ANALYSE COMPARATIVE RÉGIONALE Le tableau ci-dessous consolide les indicateurs disponibles pour les huit march s de comparaison retenus. Les donn es NIR proviennent de la Banque Mondiale (GFDD.EI.03) ; les taux de bancarisation croisent les donn es BAM, FMI et Banque Mondiale 2024. Pays NIR / Total Bancarisation 2024 Frais transferts R gulation frais Maroc 40,3 % (2021) 58 % ~3–4 % (r form BAM) Mod r — socle GPBM 2006 + BAM actif Tunisie ~42–45 % (est.) ~45 % ~8 % ( lev ) Faible — peu contraignant Égypte En hausse ~37 % 5–7 % En renforcement post-2022 S n gal 35,7–42,5 % ~54 % (UEMOA) 3–5 % (BCEAO) Mod r — BCEAO harmonis Côte d'Ivoire ~48–55 % (est.) ~41 % 3–5 % (BCEAO) Mod r — même cadre BCEAO Kenya ~38–42 % ~79 % ~4–6 % Fort — CBK très actif Jordanie ~35–38 % ~43 % 4–6 % Mod r — CBJ encadre Afrique du Sud 40,9 % (2021) >80 % N/A (march mature) Fort — SARB + NCA Sources : World Bank GFDD/FRED, McKinsey African Banking 2026, BAM, BCT, BCEAO, CBK, estimations M3T Consulting. 3.1 Le Maroc en position interm diaire Avec 40,3 % de NIR sur total revenus, le Maroc se positionne dans le tier sup rieur de la r gion, au même niveau que l'Afrique du Sud (40,9 %), mais en dessous des march s UEMOA (Côte d'Ivoire, S n gal historique) où la part NIR peut atteindre 55 %. Par rapport à la Tunisie, le Maroc pr sente une meilleure r gulation des frais sur transferts — r sultat direct de l'action volontariste de Bank Al-Maghrib, qui a divis par deux ces frais, là où la Tunisie maintient un taux de 8 % d favorable aux expatri s. 3.2 Le modèle kenyan : r f rence en matière d'inclusion Le Kenya affiche un taux de bancarisation de ~79 % avec une part NIR similaire au Maroc (~38–42 %). Ce paradoxe apparent s'explique par la strat gie proactive de la Central Bank of Kenya (CBK) : l'exon ration temporaire des frais M-Pesa pendant la pand mie (2020–2021) a acc l r l'adoption digitale massive. La leçon : la r duction cibl e de frais sur un vecteur d'accès privil gi (mobile) peut produire un effet de bascule sur la bancarisation, ind pendamment du niveau global de NIR. 3.3 La zone UEMOA : niveau NIR lev , bancarisation faible La Côte d'Ivoire et le S n gal affichent historiquement les parts NIR les plus lev es de l' chantillon, dans des march s où la bancarisation reste inf rieure à 55 %. Ce constat illustre l'effet de segmentation : les frais lev s concentrent les revenus sur une clientèle captive (salari s du secteur formel, entreprises) tout en excluant les m nages à revenus irr guliers. IMPACT DES FRAIS SUR LE TAUX DE BANCARISATION 4.1 Les donn es macroscopiques (BAM 2024) Le taux de bancarisation au Maroc s' tablit à 58 % à fin 2024, contre 53 % stable de 2020 à 2022 — un plafonnement structurel sur trois ans malgr la dynamique d mographique. Cette stagnation est partiellement corr l e à la persistance de frais qui rigent un seuil d'entr e conomique pour les m nages à faible revenu. Taux de bancarisation 2024 Primo-bancaris s 2024 Comptes bancaires (total) 58 % (+4 pts vs 2023) 883 579 personnes 38,2 millions (+5,2 %) Hommes : 70 % | Femmes : 46 % 55 % hommes | 45 % femmes Recul ouvertures : -6,1 % Source : Bank Al-Maghrib — Statistiques bancaires 2024. ⚠ Signal d'alerte : le recul de -6,1 % du nombre total de comptes ouverts en 2024, malgr la hausse du nombre de primo-bancaris s, traduit une rationalisation des comptes multiples. Les Marocains ferment des comptes secondaires pour r duire leurs charges de tenue de compte — preuve directe de l'impact des frais sur les comportements bancaires. 4.2 Cartographie des obstacles li s aux frais Obstacle identifi M canisme d'impact Intensit (Maroc) Frais de tenue de compte Coût fixe mensuel dissuasif pour faibles revenus ●●●○○ Mod r e Frais de carte bancaire Repr sente 10–15 % du SMIG mensuel pour une carte Classic ●●●●○ Élev e Frais de virement hors place P nalise les zones rurales loign es d'agences ●●●●○ Élev e Commission de change Obstacle pour les MRE / travailleurs transfrontaliers ●●○○○ Faible (r form ) Frais interbancaires (CMI) Rench rit le paiement lectronique vs. cash ●●●○○ En baisse (2025) Complexit documentaire Frais implicites (temps, d placements, justificatifs) ●●●●● Très lev e M fiance institutionnelle Frein culturel amplifi par perception de frais injustifi s ●●●●○ Élev e Lecture : ●●●●● = obstacle très lev ; ○○○○○ = obstacle n gligeable. 4.3 Effets diff renci s par segment de population L'impact des frais sur la bancarisation n'est pas uniforme. Quatre segments sont particulièrement expos s : Segment Sp cificit de l'impact Indicateur de r f rence Femmes Frais de carte et tenue de compte repr sentent une part plus importante du revenu disponible (revenus moyens inf rieurs, emploi informel pr pond rant) Bancarisation femmes : 46 % vs 70 % hommes (2024) Zones rurales Frais de d placement implicites (accès agence) + frais de virement lev s. Le cash reste le mode dominant par d faut conomique. < 1 agence pour 10 000 habitants en zone rurale (BAM 2023) Jeunes 18–25 ans Primo-entrants sans revenus stables : coût annuel carte + tenue de compte (~400–500 MAD/an) constitue un frein à l'entr e 55 % des primo-bancaris s 2024 ont moins de 25 ans MRE / diaspora Frais de transferts impactent volume d'envois et recours aux canaux formels vs. informels R forme BAM : effet positif mesurable sur part du canal bancaire RÉFORMES EN COURS ET LEVIERS STRATÉGIQUES Consciente de ces freins, Bank Al-Maghrib a engag depuis 2019 une s rie de r formes cibl es dont l'efficacit commence à produire des effets mesurables. Elles s'articulent autour de quatre axes : 5.1 Strat gie Nationale d'Inclusion Financière — SNIF 2019–2027 La SNIF Phase 1 (2019–2023) a permis le renforcement du cadre l gal (loi sur les tablissements de paiement), le d veloppement des comptes de paiement simplifi s, et l' ducation financière. La Phase 2 (2024–2027) met explicitement l'accent sur la r duction des frais de transaction comme levier d'inclusion. Objectif d clar : atteindre 75 % de bancarisation à horizon 2027 Levier cl : comptes de paiement à coût minimal pour les populations à faible revenu Éducation financière : programme SNIF int grant la transparence des frais 5.2 Ouverture du march des paiements (2025) Fin 2024, le Conseil de la Concurrence a mis fin au quasi-monopole du Centre Mon tique Interbancaire (CMI), ouvrant le march marocain des paiements lectroniques à la concurrence effective dès le 1er mai 2025. BAM a parallèlement plafonn la commission interbancaire à 0,65 % de la valeur de la transaction. 5.3 Digital Morocco 2030 Le plan Digital Morocco 2030 (lanc septembre 2024) vise à faire du paiement mobile un pilier de la transformation num rique nationale. La digitalisation des paiements de l'État (protection sociale, allocations) r duit structurellement la d pendance au cash et cr e un point d'entr e bancaire pour des m nages auparavant exclus. 5.4 Benchmarks de bonnes pratiques r gionales Pays Mesure R sultat / Impact Kenya Exon ration temporaire frais M-Pesa (2020–2021, CBK) + compte M-Shwari à frais nuls Passage de ~50 % à ~79 % de bancarisation en 5 ans Rwanda Compte bancaire de base gratuit impos par la BNR à toutes les banques commerciales Bancarisation +30 pts en 7 ans (20 % → 50 %+) UEMOA Harmonisation BCEAO des plafonds de commissions sur transferts et mon tique Mobile money : 35–50 % des adultes en zone UEMOA Égypte Compte national (Meeza card) à frais minimaux — programme BCÉ 2022+ + 8 millions de nouveaux comptes en 2 ans RECOMMANDATIONS STRATÉGIQUES Sur la base de l'analyse comparative et des benchmarks identifi s, M3T Consulting formule les recommandations suivantes, articul es selon les trois niveaux d'action (r gulateur, secteur bancaire, État) : A — Niveau r gulateur (Bank Al-Maghrib / GPBM) Étendre le p rimètre des services gratuits : inclure les virements digitaux intrabanque et le relev lectronique dans le socle GPBM obligatoire Instaurer un Compte de Base Inclusif (CBI) : compte à tenue gratuite, carte de paiement à tarif social (< 60 MAD/an), virement lectronique inclus — à l'image du modèle rwandais Renforcer la transparence tarifaire : publication comparative trimestrielle BAM accessible en ligne et en agence Acc l rer la supervision des frais interbancaires post-CMI : suivi ex-post des effets de l'ouverture 2025 sur les tarifs r percut s aux consommateurs B — Niveau secteur bancaire ( tablissements) D velopper des offres segment es à tarification sociale : formules jeunes (< 25 ans) et femmes sans emploi avec tenue de compte gratuite pendant 24 mois Digitaliser la facturation : migration des op rations courantes vers le digital sans frais additionnels D ployer les agents bancaires en zones rurales : modèle d'agent banking r duisant les frais implicites de d placement Former les quipes front-office à l'explication des frais : r duire la m fiance par la transparence relationnelle C — Niveau État / politique publique Acc l rer la digitalisation des paiements sociaux (AMO, allocations, indemnit s) : cr e un ancrage bancaire obligatoire pour des millions de m nages non-bancaris s Conditionner l'accès aux march s publics et aux subventions à la domiciliation bancaire des TPE Inclure les frais bancaires dans l' ducation financière nationale : programmes ciblant les femmes rurales, les jeunes et les TPE VII. CONCLUSION Le Maroc occupe une position interm diaire dans le paysage bancaire r gional : ses frais hors int rêts sont significatifs (NIR ~40 % du total revenus) mais mieux r gul s que la Tunisie sur les transferts, comparables à l'Afrique du Sud sur la structure globale, et moins lev s que les march s UEMOA sur les commissions de services. Les frais bancaires constituent un frein r el et document à la bancarisation des segments vuln rables — femmes, zones rurales, jeunes sans revenus stables — et leur r duction cibl e repr sente l'un des leviers les plus directs disponibles pour franchir le seuil symbolique de 75 % fix par la SNIF. Les exp riences du Kenya, du Rwanda et de l'Égypte d montrent qu'un compte de base à coût minimal ou nul peut produire des effets d'inclusion massifs en quelques ann es. L'enjeu pour les banques marocaines est de r concilier deux imp ratifs : la rentabilit des revenus non-int rêts (indispensable à la solidit du secteur) et l'accessibilit tarifaire (n cessaire à l'approfondissement du march domestique). Ces deux objectifs ne sont pas contradictoires : un march bancaris à 75 % g nère structurellement plus de revenus qu'un march bloqu à 58 %. ◆ Conclusion analytique M3T : La r duction des frais bancaires hors int rêts n'est pas un sacrifice de rentabilit — c'est un investissement dans le march adressable. Les banques marocaines qui d velopperont les offres inclusives les plus comp titives captureront en premier les 11 millions d'adultes marocains encore non-bancaris s. C'est la logique du « profit through inclusion » qui transforme l'objectif r glementaire en opportunit strat gique. ANNEXE A — GLOSSAIRE DES TERMES TECHNIQUES Les termes ci-dessous sont d finis dans leur acception sp cifique au contexte de cette analyse. Ils sont list s par ordre alphab tique pour une consultation ais e. Terme D finition complète Bancarisation Taux de la population adulte disposant d'au moins un compte bancaire actif dans un tablissement de cr dit agr . Au Maroc, mesur et publi annuellement par Bank Al-Maghrib sur la base des donn es de la Centrale des comptes bancaires. Ne comprend pas les comptes de paiement mobile non rattach s à une banque. BCEAO (Banque Centrale des États de l'Afrique de l'Ouest) Institut d' mission commun des huit États membres de l'UEMOA (B nin, Burkina Faso, Côte d'Ivoire, Guin e-Bissau, Mali, Niger, S n gal, Togo). R gule et supervise les banques et tablissements financiers de la zone franc CFA, et harmonise la politique tarifaire sur les op rations bancaires transfrontalières. CMI (Centre Mon tique Interbancaire) Op rateur technique qui assurait jusqu'au 1er mai 2025 le quasi-monopole du traitement des paiements lectroniques interbancaires au Maroc (TPE, DAB, paiements en ligne). Sa position dominante a t remise en cause par le Conseil de la Concurrence fin 2024, ouvrant le march à de nouveaux entrants et à une comp tition sur les commissions d'interchange. Commission d'interchange Frais perçus par la banque mettrice de la carte bancaire auprès de la banque acqu reuse (celle du commerçant) lors de chaque transaction. Au Maroc, BAM a plafonn cette commission à 0,65 % de la valeur de la transaction en 2024, interdisant par ailleurs sa refacturation directe au consommateur final. FRED (Federal Reserve Economic Data) Base de donn es conomiques publique g r e par la Banque de R serve F d rale de St. Louis, qui h berge et diffuse l'ensemble des s ries statistiques du Global Financial Development Database (GFDD) de la Banque Mondiale. L'indicateur utilis dans cette analyse — GFDD.EI.03 — est accessible via les s ries DDEI03MAA156NWDB (Maroc) et quivalents pays. GFDD (Global Financial Development Database) Base de donn es produite par la Banque Mondiale mesurant le d veloppement financier de ~200 pays sur 4 dimensions : profondeur, accès, efficience et stabilit . L'indicateur GFDD.EI.03 mesure la part des revenus non-int rêts dans le total des revenus bancaires (NII + NIR), calcul à partir des donn es Bankscope sur donn es non consolid es. GPBM (Groupement Professionnel des Banques du Maroc) Organisation professionnelle f d rant l'ensemble des banques marocaines agr es. Interlocuteur de Bank Al-Maghrib pour la n gociation des conventions tarifaires, notamment l'accord de 2006 instituant la gratuit des services bancaires de base (ouverture de compte, ch quier, relev mensuel, versements d'espèces). Inclusion financière Accès de l'ensemble de la population — y compris les segments vuln rables (femmes, populations rurales, jeunes, TPE) — à des services financiers formels utiles et abordables : comptes de transaction, pargne, cr dit, paiement et assurance. Mesur e par la Banque Mondiale via l'indice Global Findex (enquête triennale). MRE (Marocains R sidant à l'Étranger) Diaspora marocaine tablie hors du Maroc, constituant un segment strat gique pour les banques marocaines (comptes devises, transferts de fonds). Les transferts MRE repr sentent environ 9–10 % du PIB marocain. La r forme des frais de transferts impuls e par BAM a directement b n fici à ce segment, r duisant le coût de rapatriement des fonds. NII (Net Interest Income) Revenu net d'int rêts : diff rentiel entre les produits g n r s par les cr dits accord s (int rêts perçus) et les charges pay es sur les d pôts collect s (int rêts vers s). Principal pilier de revenu des banques de d tail dans les march s mergents, compl mentaire au NIR. NIR (Non-Interest Revenue) Revenus bancaires hors int rêts, galement appel s revenus de commissions ou frais de services. Comprennent : commissions sur op rations (virements, chèques, cartes), frais de tenue de compte, revenus de change, gains sur trading et d riv s, produits sur services d'assurance et de banque de financement. Objet central de cette analyse. SNIF (Strat gie Nationale d'Inclusion Financière) Programme strat gique lanc en 2019 conjointement par Bank Al-Maghrib et le gouvernement marocain, structur en deux phases : Phase 1 (2019–2023) ax e sur le cadre l gal et les produits inclusifs ; Phase 2 (2024–2027) centr e sur la r duction des frais de transaction, l'infrastructure num rique et l' ducation financière. Objectif : porter le taux de bancarisation à 75 % d'ici 2027. TPE / TPME Très Petite Entreprise (TPE) et Très Petite et Moyenne Entreprise (TPME) : segment entrepreneurial prioritaire de la SNIF en matière d'accès au financement bancaire. Au Maroc, environ 88 % des PME restent sous-bancaris es selon les estimations sectorielles. Le programme Intelaka (6,8 Mds MAD distribu s en 2023) constitue le principal levier public de bancarisation de ce segment. UEMOA (Union Économique et Mon taire Ouest-Africaine) Zone d'int gration conomique et mon taire regroupant 8 pays d'Afrique de l'Ouest partageant le franc CFA BCEAO. Dispose d'un cadre r glementaire bancaire harmonis g r par la BCEAO, incluant des plafonds de commissions interbancaires et des règles de protection des consommateurs de services financiers. ANNEXE B — RÉFÉRENCES ET SOURCES AVEC LIENS ACTIFS RÉGULATEURS & BANQUES CENTRALES [1] Bank Al-Maghrib — Statistiques bancaires & comptes 2024 Donn es officielles sur le taux de bancarisation, nombre de comptes, primo-bancaris s 2024. [2] Bank Al-Maghrib — Rapports sur les infrastructures des march s financiers et moyens de paiement 2024 Strat gie nationale des paiements, cadre r glementaire CMI et paiements lectroniques. [3] Bank Al-Maghrib — Documents de travail de recherche 2024 Études conom triques sur les chocs de cr dit et la financiarisation de l' conomie marocaine. [4] Banque Centrale de Tunisie (BCT) — Tableau comparatif des frais bancaires Observatoire de l'Inclusion Financière de la BCT : comparatif tarifaire des banques tunisiennes. BANQUE MONDIALE & INSTITUTIONS MULTILATÉRALES [5] World Bank FRED — NIR/Total Income Maroc (DDEI03MAA156NWDB) S rie temporelle complète de l'indicateur GFDD.EI.03 pour le Maroc (2010–2021). [6] World Bank FRED — NIR/Total Income S n gal (DDEI03SNA156NWDB) Même indicateur pour le S n gal — base de comparaison UEMOA (2010–2020). [7] World Bank FRED — NIR/Total Income Afrique du Sud (DDEI03ZAA156NWDB) R f rence march mature africain (40,9 % en 2021). [8] FMI — Article IV Consultation Maroc 2024 (Staff Country Report 2024/099) Analyse macro conomique et bancaire, transmission des taux, croissance du cr dit 2023–2024. ÉTUDES & ANALYSES SECTORIELLES [9] McKinsey Global Institute — From Potential to Performance: A Snapshot of African Banking (mars 2026) Analyse des 5 march s leaders africains dont le Maroc. ROE, NIR vs NII, croissance 2024–2025. [10] MDPI Journal of Risk & Financial Management — Non-Interest Income in MENA Region Banks (mars 2024) Étude acad mique sur l'impact des revenus non-int rêts sur la rentabilit des banques MENA (40 banques, 2010–2022). [11] African Business — Africa's Top 100 Banks 2025 Classement et analyse des grandes banques africaines dont Attijariwafa Bank (3ème, Tier 1 capital 6,2 Mds $). PRESSE ÉCONOMIQUE & DONNÉES MAROC [12] M dias 24 — Taux de bancarisation 58 % au Maroc en 2024 (juillet 2025) Analyse d taill e de l' volution m thodologique et des donn es BAM 2024. [13] Le360 — Mobile et inclusion financière au Maroc (octobre 2025) SNIF, Digital Morocco 2030, fin du monopole CMI et enjeux de l'inclusion par le mobile. [14] LesEco.ma — Bancarisation : des progrès certains, mais des d fis persistants (juillet 2024) Analyse des freins structurels à la bancarisation dont l'impact des frais sur les populations vuln rables. [15] LesEco.ma — Bancarisation : l'objectif des 75 % se pr cise (juillet 2025) Donn es 2024, rationalisation des comptes multiples, tendances comportementales. [16] FNH.ma — Strat gie nationale d'inclusion financière : bilan 5 ans (novembre 2024) Bilan de la SNIF Phase 1 et objectifs de la Phase 2 (2024–2027). [17] Le Matin — Inclusion financière : Bank Al-Maghrib acc lère ses r formes (f vrier 2026) Interview BAM sur les priorit s r glementaires : infrastructure num rique, frais, TPE. [18] Le360 — Bank Al-Maghrib acc lère sa strat gie pour r duire la d pendance au cash (d cembre 2025) Strat gie nationale des paiements BAM 2024 : commission interbancaire plafonn e à 0,65 %. [19] HAC.ma — How to Navigate Morocco's Banking and Financial System (janvier 2026) Synthèse pratique des frais bancaires marocains (change, cartes, conditions d'ouverture). [20] Babnet.tn — Baisser les frais bancaires tunisiens sur transferts à 3 % (juillet 2025) Comparaison des frais sur transferts Tunisie (~8 %) vs Maroc, S n gal, Côte d'Ivoire. © M3T Consulting 2026 — Toute reproduction partielle ou totale soumise à autorisation pr alable crite. R f rence : M3T-GRC-2026-007 v2.

by Youness El Kandoussi | 1 month ago | 0 Comment(s) | 93 Share(s) | Tags :

Abstract: Risk management is a critical aspect of any organization's success. In this comprehensive 10-page article, we delve deep into the concepts of risk management, risk appetite, risk tolerance, and risk capacity. We explore their definitions, importance, and the interplay between them. Furthermore, we discuss various strategies and best practices for effective risk mitigation in the ever-changing landscape of modern business. Table of Contents 1. Introduction 1.1. The Importance of Risk Management 1.2. Defining Key Concepts2. Understanding Risk 2.1. Types of Risk 2.2. The Risk-Reward Trade-off3. Risk Management Framework 3.1. Identifying Risks 3.2. Assessing Risks 3.3. Managing Risks4. Risk Appetite 4.1. Definition and Significance 4.2. Aligning Risk Appetite with Business Objectives5. Risk Tolerance 5.1. Determining Risk Tolerance 5.2. Balancing Risk and Reward6. Risk Capacity 6.1. Assessing Risk Capacity 6.2. Setting Boundaries7. Strategies for Effective Risk Management 7.1. Diversification 7.2. Risk Transfer 7.3. Risk Avoidance 7.4. Risk Reduction 7.5. Risk Acceptance8. Case Studies 8.1. Enron Corporation 8.2. JPMorgan Chase & the London Whale 8.3. Tesla's Risk-Taking Approach9. Risk Management in the Digital Age 9.1. Cybersecurity Risks 9.2. Data Privacy Risks10. Conclusion 10.1. The Evolving Landscape of Risk Management 10.2. The Imperative of Continuous Adaptation 1. Introduction 1.1. The Importance of Risk Management Risk is an inherent part of business operations. It can manifest in various forms, from financial and operational risks to strategic and reputational risks. Effective risk management is crucial for organizations to not only survive but thrive in a volatile, uncertain, complex, and ambiguous (VUCA) world. Without proper risk management strategies in place, organizations are vulnerable to unexpected setbacks and potential crises. 1.2. Defining Key Concepts Before diving into risk management strategies, it's essential to understand key concepts related to risk. These include risk appetite, risk tolerance, and risk capacity. While these terms are often used interchangeably, they each have distinct meanings and implications for an organization's risk management framework. 2. Understanding Risk 2.1. Types of Risk To effectively manage risk, one must first understand its various forms. Common types of risk include financial risk, operational risk, strategic risk, compliance risk, and reputational risk. Each of these risks poses unique challenges and requires tailored approaches to mitigation. 2.2. The Risk-Reward Trade-off Risk is not inherently negative. In fact, it is often intertwined with opportunities for growth and innovation. The concept of the risk-reward trade-off acknowledges that higher levels of risk can yield greater rewards, but they also come with increased potential for losses. Striking the right balance between risk and reward is a fundamental consideration for any organization. 3. Risk Management Framework 3.1. Identifying Risks Effective risk management begins with the identification of potential risks. This involves a comprehensive analysis of internal and external factors that could impact the organization's objectives. Risk identification is an ongoing process that requires input from all levels of the organization. 3.2. Assessing Risks Once risks are identified, they must be assessed in terms of their potential impact and likelihood. Quantitative and qualitative methods, such as risk matrices and scenario analysis, are commonly used to evaluate risks. This assessment informs the prioritization of risks for mitigation efforts. 3.3. Managing Risks Risk management involves a range of strategies to address identified risks. These strategies can include risk avoidance, risk reduction, risk transfer, risk acceptance, and diversification. The choice of strategy depends on the organization's risk appetite, tolerance, and capacity. 4. Risk Appetite 4.1. Definition and Significance Risk appetite is the level of risk an organization is willing to accept in pursuit of its objectives. It is a fundamental component of an organization's risk management framework as it sets the tone for how much risk is considered acceptable. Risk appetite should align with an organization's strategic goals and values. 4.2. Aligning Risk Appetite with Business Objectives To effectively manage risk, an organization's risk appetite must align with its business objectives. For example, a tech startup seeking rapid growth may have a higher risk appetite, while a well-established financial institution may prioritize stability and have a lower risk appetite. Balancing risk appetite with risk tolerance is critical to avoid taking unnecessary risks or stifling innovation. 5. Risk Tolerance 5.1. Determining Risk Tolerance Risk tolerance is the degree of risk an organization is willing to endure before taking corrective action. It is often measured in terms of specific metrics, such as financial losses or project delays. Determining risk tolerance involves evaluating the organization's financial capacity to withstand losses and its willingness to take risks. 5.2. Balancing Risk and Reward Balancing risk tolerance with risk appetite is essential for maintaining a healthy risk management framework. An organization must strike a balance between pursuing opportunities that align with its risk appetite and ensuring that it does not exceed its risk tolerance, which could lead to catastrophic consequences. 6. Risk Capacity 6.1. Assessing Risk Capacity Risk capacity is the maximum amount of risk an organization can afford to take without jeopardizing its viability. It takes into account the organization's financial resources, capital reserves, and overall financial health. Assessing risk capacity involves evaluating the organization's ability to absorb losses without severe consequences. 6.2. Setting Boundaries Establishing clear boundaries for risk capacity is crucial for avoiding overexposure to risk. These boundaries serve as safeguards to prevent an organization from taking on more risk than it can handle. Effective risk capacity management ensures the organization's long-term sustainability. 7. Strategies for Effective Risk Management 7.1. Diversification Diversification involves spreading investments or operations across a variety of assets or markets. This strategy reduces the impact of a single risk event on the overall portfolio. Diversifying across different industries, geographic regions, or asset classes can mitigate risks associated with economic fluctuations. 7.2. Risk Transfer Risk transfer involves shifting the financial burden of a risk to another party, typically through insurance or contractual agreements. This strategy can be particularly effective for mitigating specific risks, such as liability or property damage. 7.3. Risk Avoidance Risk avoidance entails eliminating activities or investments that carry unacceptable levels of risk. While this strategy can be effective for high-impact, low-probability risks, it may also limit growth opportunities. 7.4. Risk Reduction Risk reduction involves implementing measures to decrease the likelihood or impact of a risk. This may include enhanced security protocols, process improvements, or disaster preparedness plans. 7.5. Risk Acceptance In some cases, organizations may choose to accept certain risks when the potential benefits outweigh the potential losses. Risk acceptance should be a conscious and informed decision, with contingency plans in place. 8. Case Studies 8.1. Enron Corporation The Enron Corporation scandal serves as a cautionary tale of the consequences of failing to manage financial and operational risks adequately. Enron's aggressive risk-taking and lack of transparency ultimately led to its downfall and the loss of billions of dollars for investors. 8.2. JPMorgan Chase & the London Whale The JPMorgan Chase "London Whale" incident highlights the importance of risk monitoring and control. In this case, a trader's risky bets resulted in massive losses for the bank, illustrating the need for robust risk management systems. 8.3. Tesla's Risk-Taking Approach Tesla's ambitious approach to electric vehicle innovation and market disruption showcases the potential rewards of a high-risk, high-reward strategy. Elon Musk's willingness to take substantial risks has propelled Tesla to a dominant position in the electric vehicle industry. 9. Risk Management in the Digital Age 9.1. Cybersecurity Risks The digital age has introduced new and complex risks, particularly in the realm of cybersecurity. Organizations must invest in robust cybersecurity measures to protect sensitive data and infrastructure from cyber threats. 9.2. Data Privacy Risks With the proliferation of data collection and storage, data privacy risks have become a significant concern. Organizations must navigate a web of regulations and consumer expectations to safeguard personal data. 10. Conclusion 10.1. The Evolving Landscape of Risk Management In conclusion, risk management is a dynamic and essential practice for organizations of all sizes and industries. Understanding the concepts of risk appetite, risk tolerance, and risk capacity is fundamental to building a resilient risk management framework. Moreover, the strategies discussed in this article provide valuable insights into mitigating risks and seizing opportunities. 10.2. The Imperative of Continuous Adaptation As the business environment continues to evolve, so too must an organization's approach to risk management. Flexibility, adaptability, and a commitment to staying informed about emerging risks are crucial for navigating the complex and ever-changing landscape of risk management. Incorporating these principles and strategies into your organization's risk management framework will enhance its ability to thrive in the face of uncertainty, ultimately ensuring a more secure and prosperous future. This article provides a comprehensive overview of risk management, risk appetite, risk tolerance, and risk capacity. It explores their definitions, significance, and practical implications for organizations. Additionally, it delves into various strategies and case studies, offering a well-rounded perspective on the complex world of risk management. References and Sources [1] COSO. (2013). Enterprise risk management: Integrating with strategy and performance. Committee of Sponsoring Organizations of the Treadway Commission. [2] Project Management Institute. (2017). A guide to the project management body of knowledge (PMBOK Guide) (6th ed.). Project Management Institute. [3] International Organization for Standardization. (2018). ISO 31000:2018 Risk management. International Organization for Standardization. [4] National Institute of Standards and Technology. (2021). Cybersecurity framework: Version 1.1. National Institute of Standards and Technology. [5] General Data Protection Regulation (EU) 2016/679. Official Journal of the European Union. Specific References [1.1] "Without proper risk management strategies in place, organizations are vulnerable to unexpected setbacks and potential crises." (COSO, 2013) [2.2] "The concept of the risk-reward trade-off acknowledges that higher levels of risk can yield greater rewards, but they also come with increased potential for losses." (Project Management Institute, 2017) [3.1] "Risk identification is an ongoing process that requires input from all levels of the organization." (International Organization for Standardization, 2018) [4.1] "Risk appetite is the level of risk an organization is willing to accept in pursuit of its objectives." (COSO, 2013) [4.2] "An organization's risk appetite must align with its business objectives." (International Organization for Standardization, 2018) [5.1] "Determining risk tolerance involves evaluating the organization's financial capacity to withstand losses and its willingness to take risks." (Project Management Institute, 2017) [5.2] "Balancing risk tolerance with risk appetite is essential for maintaining a healthy risk management framework." (COSO, 2013) [6.1] "Assessing risk capacity involves evaluating the organization's ability to absorb losses without severe consequences." (National Institute of Standards and Technology, 2021) [6.2] "Establishing clear boundaries for risk capacity is crucial for avoiding overexposure to risk." (International Organization for Standardization, 2018) [7.1] "Diversification reduces the impact of a single risk event on the overall portfolio." (Project Management Institute, 2017) [7.2] "Risk transfer can be particularly effective for mitigating specific risks, such as liability or property damage." (COSO, 2013) [7.3] "While risk avoidance can be effective for high-impact, low-probability risks, it may also limit growth opportunities." (National Institute of Standards and Technology, 2021) [7.4] "Risk reduction may include enhanced security protocols, process improvements, or disaster preparedness plans." (International Organization for Standardization, 2018) [7.5] "Risk acceptance should be a conscious and informed decision, with contingency plans in place." (Project Management Institute, 2017) [8.1] "Enron's aggressive risk-taking and lack of transparency ultimately led to its downfall and the loss of billions of dollars for investors." (COSO, 2013) [8.2] "The JPMorgan Chase 'London Whale' incident highlights the importance of risk monitoring and control." (National Institute of Standards and Technology, 2021) [8.3] "Elon Musk's willingness to take substantial risks has propelled Tesla to a dominant position in the electric vehicle industry." (Project Management Institute, 2017) [9.1] "Organizations must invest in robust cybersecurity measures to protect sensitive data and infrastructure from cyber threats." (General Data Protection Regulation, 2016) [9.2] "Organizations must navigate a web of regulations and consumer expectations to safeguard personal data." (National Institute of Standards and Technology, 2021) [10.1] "The digital age has introduced new and complex risks, particularly in the realm of cybersecurity." (Project Management Institute, 2017) [10.2] "Understanding the concepts of risk appetite, risk tolerance, and risk capacity is fundamental to building a resilient risk management framework." (COSO, 2013) Photo credits to http://www.criscexamstudy.com/

by Youness El Kandoussi | 2 years ago | 0 Comment(s) | 1690 Share(s) | Tags :

POST COMMENT

COMMENTS(0)

No Comment yet. Be the first :)