ABOUT AUTHOR

CATEGORIES

READ ALSO

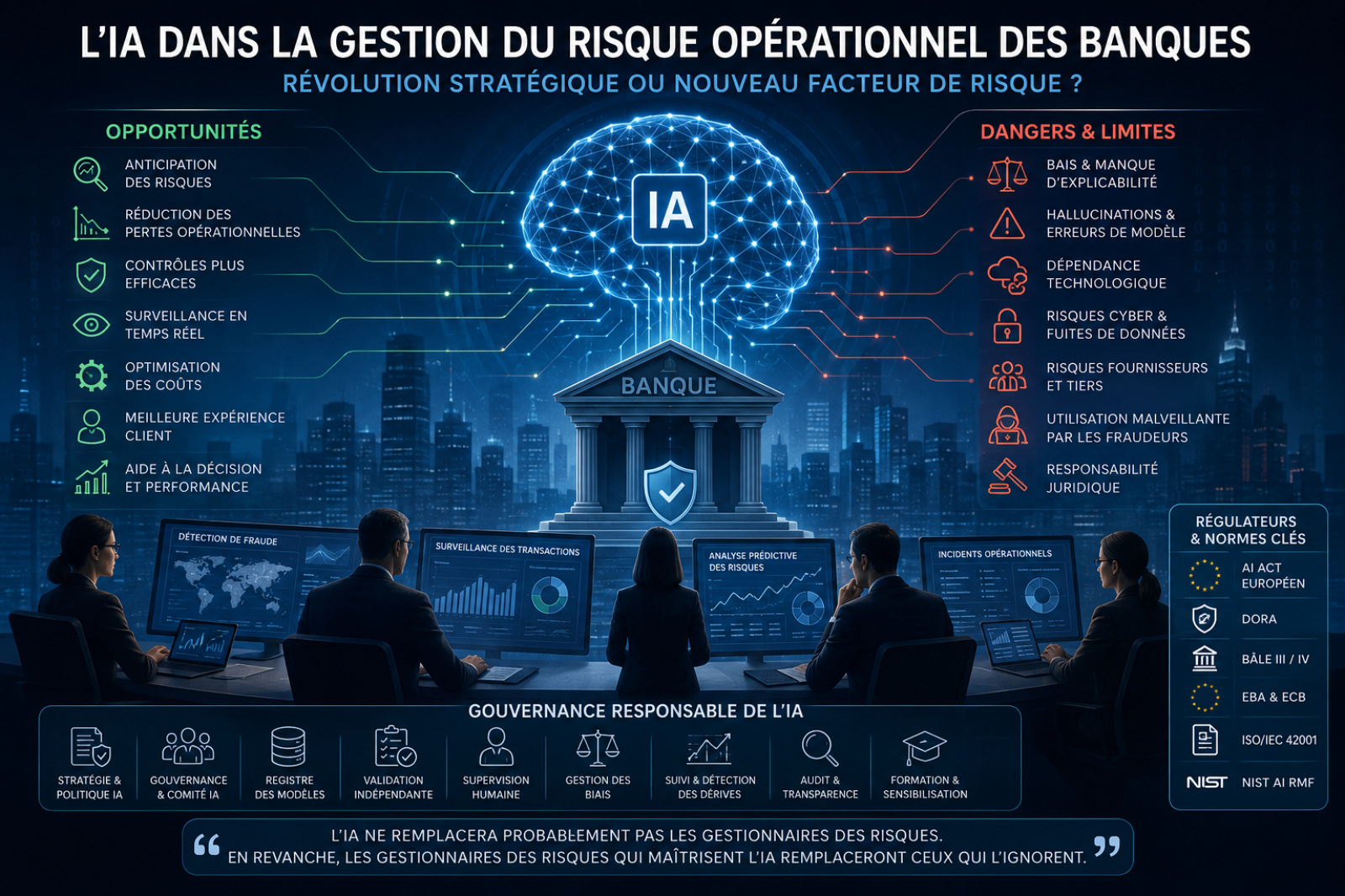

Comment construire une gouvernance de l'IA qui inspire confiance, respecte les exigences r glementaires et cr e un avantage concurrentiel durable. Une salle des march s qui ne dort jamais Il y a dix ans, un incident op rationnel majeur mettait plusieurs heures à être d tect . Aujourd'hui, dans certaines banques, un modèle d'IA identifie une anomalie de flux de paiement en quelques secondes, la corrèle avec des dizaines de signaux faibles, et alerte l' quipe de contrôle permanent avant même qu'un client ne s'en aperçoive. Ce basculement n'est pas anecdotique : il red finit la nature même du m tier de gestionnaire des risques. Mais cette même technologie qui d tecte la fraude en temps r el peut aussi se tromper en toute confiance, halluciner un chiffre inexistant dans un rapport r glementaire, ou reproduire un biais discriminatoire à grande chelle. L'IA n'est donc ni un simple outil d'efficacit , ni une menace à carter par principe. C'est un nouveau territoire de risque op rationnel à part entière, qui doit être gouvern avec la même rigueur que le risque de cr dit ou le risque de march . C'est pr cis ment cette double lecture — acc l rateur de r silience et risque mergent — qui doit structurer la r flexion des dirigeants bancaires en 2026. Pourquoi l'IA devient incontournable dans les banques Plusieurs pressions convergentes expliquent l'acc l ration actuelle. La pression r glementaire s'intensifie. DORA impose depuis janvier 2025 un cadre strict de gestion du risque ICT, de reporting d'incidents et de tests de r silience op rationnelle num rique pour l'ensemble des entit s financières europ ennes. En parallèle, le règlement europ en sur l'IA (AI Act) est entr en vigueur en août 2024, avec des obligations de plus en plus contraignantes pour les systèmes d'IA à haut risque — dont plusieurs cas d'usage bancaires (scoring de cr dit, valuation de risque) relèvent directement. Les banques doivent d sormais d montrer, preuves à l'appui, qu'elles maîtrisent leurs modèles. La cybercriminalit et la fraude se sophistiquent. Selon les donn es cit es par Deloitte, les pertes li es à la fraude d'identit dans les services financiers ont atteint 12,5 milliards de dollars en 2024, en hausse de 25 % par rapport à 2023, port es notamment par les identit s synth tiques. L'activit frauduleuse aurait progress d'environ 21 % entre 2024 et 2025, avec d sormais une tentative de v rification sur vingt signal e comme potentiellement frauduleuse. Plus pr occupant encore : plus de la moiti des fraudes impliqueraient aujourd'hui une composante IA (deepfakes, identit s synth tiques, hameçonnage automatis ), un ph nomène qui pourrait porter les pertes li es à la fraude g n r e par IA à 40 milliards de dollars d'ici 2027. Les coûts op rationnels restent sous tension. McKinsey estime que les fonctions op rationnelles mobilisent entre 50 % et 60 % des quivalents temps plein d'une banque type, ce qui en fait un terrain naturel de transformation par l'IA, juste après la technologie et l'ing nierie. Les donn es explosent, et avec elles la capacit — ou l'incapacit — des banques à les exploiter en temps r el pour d tecter les signaux de risque. Les attentes des clients voluent vers une exp rience instantan e, personnalis e et sans friction, y compris dans la gestion des r clamations, des alertes de fraude ou des interactions avec les quipes de conformit . Les principaux cas d'usage dans le risque op rationnel D tection de fraude. Les moteurs de machine learning analysent des millions de points de donn es par transaction pour rep rer des sch mas anormaux, remplaçant progressivement les règles statiques historiques. D'après une enquête Mastercard men e avec Financial Times Longitude, 42 % des metteurs et 26 % des acqu reurs d clarent avoir vit plus de 5 millions de dollars de pertes de fraude sur deux ans grâce à l'IA, et 80 % des organisations estiment que l'IA a permis de r duire les contrôles manuels inutiles. Lutte contre le blanchiment (AML). Les modèles d'IA croisent des volumes massifs de transactions avec des bases de sanctions, des donn es de b n ficiaires effectifs et des sch mas comportementaux. Un exemple souvent cit dans l'industrie est celui d'un grand groupe bancaire international ayant d ploy une solution d'IA capable de surveiller plusieurs centaines de millions de transactions mensuelles sur des dizaines de millions de comptes, pour d tecter des r seaux de blanchiment que les approches traditionnelles peinaient à identifier. Surveillance des transactions et scoring des risques. Des modèles pr dictifs attribuent en continu un score de risque dynamique à chaque client, chaque transaction ou chaque contrepartie, permettant un pilotage proactif plutôt que r actif. Gestion des incidents op rationnels. Des systèmes d'IA classifient automatiquement les incidents, en valuent la s v rit , et orientent les quipes vers la bonne proc dure de rem diation — r duisant les d lais de d tection et de r solution. Analyse pr dictive et contrôles permanents. L'IA identifie des tendances de d rive avant qu'elles ne deviennent des incidents av r s, renforçant la première ligne de d fense. OCR intelligent et analyse documentaire. Les banques automatisent la lecture, la classification et l'extraction d'informations à partir de contrats, de dossiers KYC ou de justificatifs, r duisant drastiquement les d lais de traitement manuel. G n ration automatique de rapports r glementaires. Des outils d'IA g n rative assistent d sormais la r daction des rapports COREP, FINREP ou des dossiers de contrôle interne, en s'appuyant sur des donn es structur es et une supervision humaine. IA g n rative pour les quipes Risk et Compliance. Des « experts virtuels » internes permettent aux quipes de poser des questions en langage naturel sur les politiques internes, la r glementation ou l'historique des incidents, acc l rant la prise de d cision sans remplacer le jugement humain. Les opportunit s : une transformation mesurable Les gains ne sont plus th oriques. McKinsey value à environ 2 000 milliards de dollars la valeur annuelle totale que l'IA g n rative et l'analytique avanc e pourraient cr er dans le secteur bancaire mondial, en combinant productivit , r duction des risques et nouveaux revenus. Autre donn e significative : 70 % des banques commerciales auraient d jà adopt l'IA dans au moins une fonction cœur de m tier, et 78 % des tablissements ayant investi dans l'IA constateraient un retour sur investissement positif en moins de dix-huit mois. Concrètement, les opportunit s se d ploient sur plusieurs axes : Anticipation renforc e des risques, grâce à une surveillance continue plutôt que ponctuelle. R duction des pertes op rationnelles, par une d tection plus rapide et plus pr cise des anomalies. Qualit accrue des contrôles, avec une couverture exhaustive plutôt qu'un chantillonnage. Acc l ration des investigations, l'IA pr qualifiant les dossiers avant intervention humaine. Optimisation des coûts, notamment sur les tâches à faible valeur ajout e. R silience op rationnelle am lior e, condition d sormais explicitement attendue par les r gulateurs europ ens. Selon le rapport Deloitte sur l'adoption de l'IA dans les institutions financières europ ennes, 94 % des grandes banques et 62 % des petites banques utilisaient d jà l'IA g n rative en 2025, avec la d tection de fraude — AML et KYC compris — comme cas d'usage le plus r pandu, cit par 58 % des banques interrog es. Les dangers et les limites : l'envers du d cor Ces b n fices ne doivent pas occulter une r alit plus inconfortable : l'IA introduit une nouvelle classe de risques, à la fois techniques, thiques et juridiques. Les hallucinations restent un enjeu central pour l'IA g n rative : un modèle peut produire une r ponse plausible mais factuellement fausse, avec un niveau de confiance trompeur — un risque majeur lorsqu'il s'agit de rapports r glementaires. Les biais algorithmiques peuvent reproduire, voire amplifier, des discriminations historiques pr sentes dans les donn es d'entraînement, exposant la banque à un risque de non-conformit et r putationnel. Le manque d'explicabilit de certains modèles complexes complique la justification des d cisions auprès des r gulateurs, des clients et des auditeurs. La d pendance technologique et le risque fournisseur s'accroissent à mesure que les banques externalisent une partie de leurs capacit s d'IA à des tiers, cr ant une nouvelle forme de concentration du risque op rationnel. La cybers curit et la confidentialit des donn es deviennent des enjeux critiques : les modèles d'IA constituent eux-mêmes une nouvelle surface d'attaque. L'obsolescence des modèles, la d rive des performances dans le temps, et les erreurs de d cision qui en d coulent, exigent une surveillance continue plutôt qu'une validation ponctuelle. La responsabilit juridique reste souvent floue lorsqu'une d cision automatis e cause un pr judice. Une gouvernance insuffisante demeure, selon McKinsey, l'un des principaux freins à une adoption responsable : le niveau moyen de maturit en IA responsable a certes progress (de 2,0 à 2,3 sur une chelle de maturit entre 2025 et 2026), mais seul un tiers environ des organisations atteint un niveau de maturit lev en matière de strat gie et de gouvernance. Enfin, l'IA est d sormais aussi une arme entre les mains des fraudeurs — deepfakes, voix synth tiques, documents falsifi s — ce qui transforme la lutte antifraude en course technologique permanente. Ce qu'attendent les r gulateurs Le paysage r glementaire se densifie rapidement autour de l'IA bancaire : AI Act europ en : entr en vigueur en août 2024, il impose aux systèmes d'IA à haut risque — dont plusieurs usages bancaires comme le scoring de cr dit — des obligations de gestion des risques, de gouvernance des donn es, de documentation technique, de supervision humaine et de surveillance post-d ploiement. Le calendrier pr cis de mise en application de ces obligations pour le secteur financier continue d' voluer dans le cadre des discussions sur le « Digital Omnibus » europ en, ce qui impose une veille r glementaire active. DORA : en vigueur depuis janvier 2025, il impose un cadre de gestion du risque ICT, un registre des prestataires tiers, un reporting d'incidents et des tests de r silience — et couvre explicitement les systèmes d'IA en tant qu'actifs ICT. Bâle III/IV, ECB, EBA : ces cadres prudentiels intègrent progressivement des attentes sur la gouvernance des modèles, y compris ceux fond s sur l'IA, dans la continuit du risk management model existant (SR 11-7 et quivalents). ISO/IEC 42001 et NIST AI RMF : ces r f rentiels internationaux, bien que non contraignants juridiquement en Europe, deviennent des standards de facto pour structurer un système de management de l'IA et d montrer une gouvernance robuste face aux superviseurs. Le message commun de ces cadres est sans ambiguït : l'autonomie croissante des systèmes d'IA doit s'accompagner d'une supervision humaine renforc e, pas all g e. Bonnes pratiques : bâtir une gouvernance de l'IA qui inspire confiance Une gouvernance responsable de l'IA dans le risque op rationnel repose sur des piliers d sormais bien identifi s par l'industrie : Un comit IA transverse, associant Risk, Compliance, IT et m tiers, avec un mandat clair de validation des cas d'usage. Une politique IA formalis e, d finissant les usages autoris s, interdits et soumis à validation renforc e. Un registre des modèles, recensant chaque système d'IA, sa finalit , son niveau de risque, ses donn es d'entr e et son propri taire responsable. Une validation ind pendante des modèles, r alis e par une quipe distincte de celle qui les a d velopp s, incluant tests de robustesse et analyse d' quit . Une supervision humaine effective, en particulier sur les d cisions à fort impact (cr dit, fraude, conformit ). Une gestion active des biais, avec des tests r guliers sur des donn es repr sentatives. Des indicateurs de performance et de d rive, suivis dans la dur e et non uniquement lors de la mise en production. Un audit r gulier des modèles, int gr au plan d'audit interne global. Une documentation exhaustive, condition sine qua non pour satisfaire simultan ment les exigences de l'AI Act et de DORA. Un plan de formation des quipes Risk, Compliance et m tiers à la compr hension — non à l'ing nierie — des systèmes d'IA qu'elles supervisent. Le rôle du Risk Manager de demain La fonction risque op rationnel est en train de se transformer en profondeur. Le Risk Manager de demain devra conjuguer plusieurs identit s : AI Risk Manager, capable d' valuer le risque sp cifique d'un système d'IA, au-delà des cat gories traditionnelles. Data-driven Risk Manager, à l'aise avec l'exploitation de donn es massives et h t rogènes. Sp cialiste du Continuous Risk Monitoring, pilotant des dispositifs de surveillance en temps r el plutôt que des contrôles p riodiques. Acteur du Model Risk Management, appliquant aux modèles d'IA la même rigueur m thodologique que celle historiquement r serv e aux modèles de cr dit ou de march . Contributeur actif de l'AI Governance, aux côt s des fonctions juridiques, techniques et m tiers. Les comp tences attendues voluent en cons quence : compr hension des principes du machine learning, culture r glementaire IA, capacit à dialoguer avec les quipes data science, et surtout un sens critique renforc face aux r sultats produits par les systèmes automatis s. Tableau synth tique : opportunit s et risques de l'IA dans le risque op rationnel bancaire Dimension Opportunit s Risques D tection de fraude Identification en temps r el, r duction des faux positifs Fraude assist e par IA, deepfakes Conformit r glementaire Automatisation des rapports, gain de temps Hallucinations, erreurs non d tect es Prise de d cision Aide à la d cision, scoring dynamique Biais algorithmiques, manque d'explicabilit Coûts R duction des tâches manuelles à faible valeur Coûts d'impl mentation et de gouvernance lev s R silience op rationnelle Surveillance continue, d tection pr coce D pendance technologique, risque fournisseur R glementation Cadres structurants (AI Act, DORA) Complexit de mise en conformit multi-r gimes Capital humain Mont e en comp tences, nouveaux rôles R sistance au changement, dilution des responsabilit s Conclusion : une transformation à piloter, pas à subir L'Intelligence Artificielle ne constitue ni une baguette magique ni une menace existentielle pour la gestion du risque op rationnel bancaire. Elle est un acc l rateur puissant, à condition d'être encadr e par une gouvernance à la hauteur de sa capacit de transformation. L'IA ne remplacera probablement pas les gestionnaires des risques. En revanche, les gestionnaires des risques qui maîtrisent l'IA remplaceront ceux qui l'ignorent. Les tablissements qui sauront conjuguer ambition technologique, rigueur de gouvernance et conformit r glementaire ne se contenteront pas de r duire leurs pertes op rationnelles : ils construiront un avantage concurrentiel durable, fond sur la confiance. Cinq enseignements cl s L'adoption de l'IA dans le risque op rationnel bancaire n'est plus une option diff renciante : elle devient un standard de march . Les gains les plus tangibles se concentrent aujourd'hui sur la fraude, l'AML et l'automatisation des contrôles. Les risques introduits par l'IA — biais, hallucinations, d pendance fournisseur — appartiennent pleinement au p rimètre du risque op rationnel et doivent être trait s comme tels. AI Act et DORA imposent d sormais un double cadre de conformit qui exige une documentation et une gouvernance int gr es, et non juxtapos es. Le Risk Manager de demain sera autant un expert en gouvernance qu'un interlocuteur cr dible des quipes data et technologie. Et vous, où en est votre organisation dans la structuration de sa gouvernance IA appliqu e au risque op rationnel ? Quels cas d'usage avez-vous d jà d ploy s, et quels obstacles rencontrez-vous ? Partagez votre retour d'exp rience en commentaire — cet change nourrit une r flexion collective dont notre secteur a besoin. Sources cit es : McKinsey & Company (State of AI Trust 2026 ; Global Banking Annual Review 2026 ; Banking’s AI angst) ; Deloitte (AI Adoption in Financial Institutions — EMEA MRM Survey 2025 ; 2026 Banking & Capital Markets Outlook) ; Mastercard / Financial Times Longitude (2025 Payment Fraud Prevention Report) ; Commission europ enne (AI Act) ; r glementation DORA (UE 2022/2554).

by Youness El Kandoussi | 1 month ago | 0 Comment(s) | 70 Share(s) | Tags :

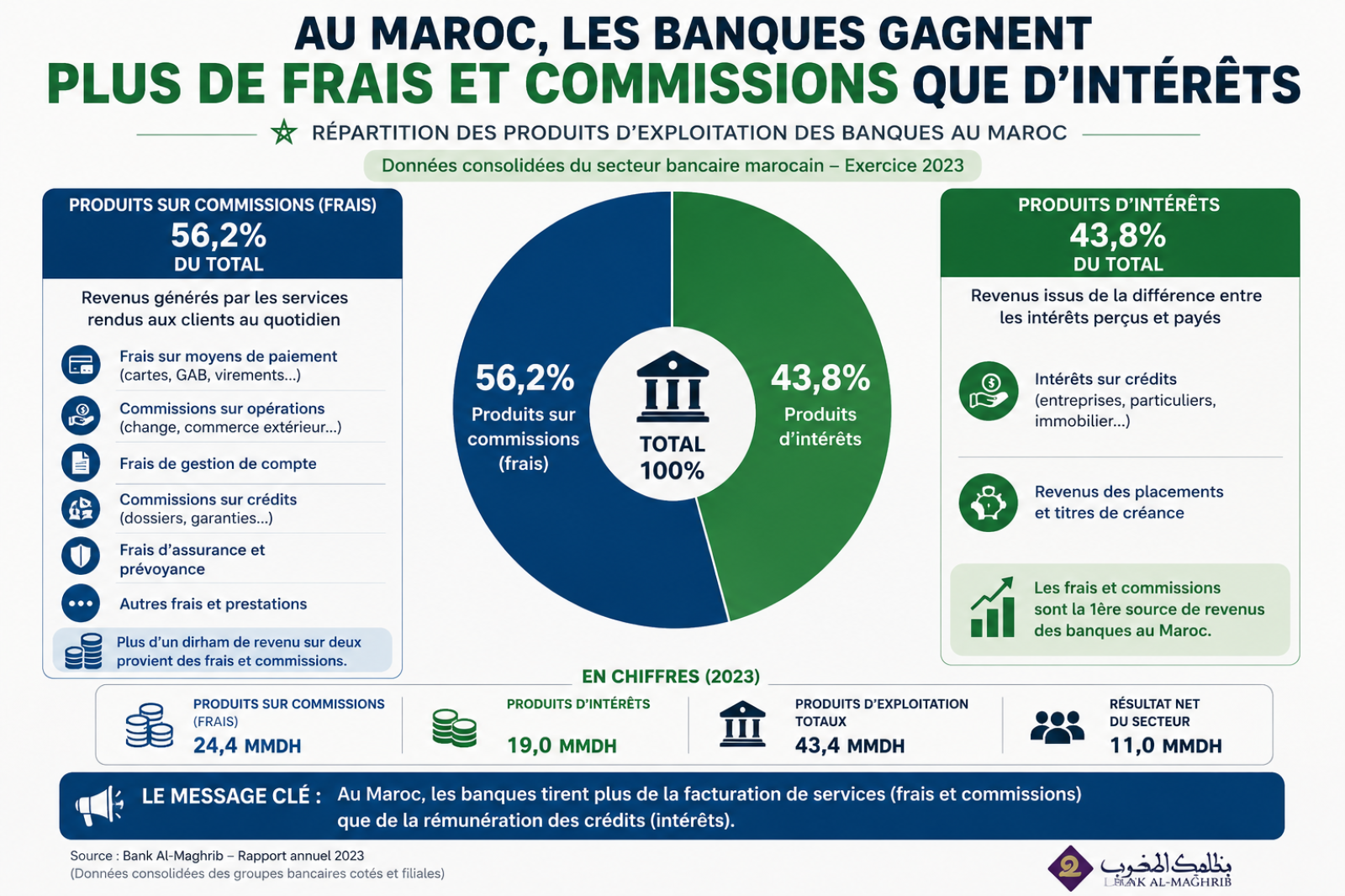

CONTEXTE ET CADRE DE L'ANALYSE Le modèle de revenus des banques commerciales repose sur deux piliers structurels : le revenu net d'int rêts (NII) — diff rentiel entre taux prêteurs et d posants — et les revenus hors int rêts (Non-Interest Revenue, NIR), qui agrègent commissions, frais de services, gains sur change, revenus de trading et autres charges factur es à la clientèle. Cette analyse porte exclusivement sur le second pilier. Dans les march s mergents d'Afrique et du Moyen-Orient, les frais et commissions bancaires constituent à la fois un levier de rentabilit pour les tablissements et un facteur de friction pour l'accès aux services financiers des m nages. Le Maroc, en tant qu' conomie mergente de r f rence en Afrique du Nord et sub-saharienne, offre un terrain d'analyse particulièrement pertinent. 1.1 P rimètre de comparaison L'analyse retient comme pays comparables ceux pr sentant des similarit s structurelles avec le Maroc selon les critères suivants : Revenu interm diaire inf rieur ou sup rieur (classification Banque Mondiale) Taux de bancarisation inf rieur à 80 % (march s d'inclusion en cours) Pr sence d'un secteur bancaire r gul et d'une banque centrale op rationnelle Proximit g ographique ou d'int gration r gionale : Afrique du Nord, Afrique subsaharienne francophone, Proche-Orient mergent Les pays retenus sont : Tunisie, Égypte, S n gal, Côte d'Ivoire, Kenya, Jordanie et, pour r f rence r gionale haute, l'Afrique du Sud. 1.2 M thodologie et sources Les donn es mobilis es proviennent des sources institutionnelles suivantes, toutes accessibles via les liens actifs de la section R f rences en fin de document : Banque Mondiale — Global Financial Development Database (GFDD/FRED) : indicateur GFDD.EI.03 (Non-Interest Income / Total Income) Bank Al-Maghrib (BAM) — Rapports annuels sur les statistiques bancaires 2023–2024 FMI — Article IV Consultation Maroc 2024 McKinsey Global Institute — « From Potential to Performance: African Banking » (mars 2026) Banque Centrale de Tunisie (BCT), BCEAO, donn es sectorielles publi es Grilles tarifaires officielles GPBM / banques marocaines (2025) STRUCTURE DES FRAIS BANCAIRES AU MAROC 2.1 Un socle de gratuit r glement e depuis 2006 Depuis l'accord de 2006 entre le Groupement Professionnel des Banques du Maroc (GPBM) et Bank Al-Maghrib, un socle minimal de services est fourni gratuitement à la clientèle : ouverture et clôture de compte, d livrance de ch quier, envoi mensuel de relev s, versements d'espèces au guichet. Cette d cision a constitu un premier levier d'inclusion, mais son p rimètre reste limit face à l' tendue r elle des charges factur es. 2.2 Grille tarifaire — Principales cat gories (2025) Cat gorie de frais Fourchette (MAD) R gime r glementaire Tenue de compte (particulier) 180 – 300 MAD/an Encadr GPBM/BAM Carte bancaire Visa Classic 120 – 180 MAD/an Tarification libre Virement hors place (agence) 15 – 40 MAD/op r. Non plafonn Virement via digital Gratuit – 10 MAD Encourag (SNIF) Opposition sur chèque 150 – 200 MAD Non plafonn Attestation / Certificat bancaire 50 – 100 MAD Non plafonn Commission de change (devises) 1 – 3 % du montant Encadr BAM Commission paiement lectronique 0,65 % transaction Plafonn BAM 2024 Retrait interbancaire (autre r seau) 5 – 15 MAD/op r. Encadr CMI → ouvert 2025 Frais de rejet (chèque sans provision) 200 – 400 MAD Barème l gal Ouverture de compte Gratuit Accord GPBM 2006 Clôture de compte Gratuit Accord GPBM 2006 Source : Grilles tarifaires GPBM, Attijariwafa Bank, Banque Populaire, CIH, BMCE — 2025. 2.3 Évolution de la part NIR/Total revenus (World Bank GFDD.EI.03) Ann e 2017 2018 2019 2020 2021 NIR / Total revenus 38,4 % 36,9 % 39,9 % 38,4 % 40,3 % Source : World Bank Global Financial Development Database — FRED Series DDEI03MAA156NWDB. ◆ Lecture analytique : Une part NIR de 40 % signifie que, pour 100 MAD de revenu bancaire total, 40 MAD proviennent de frais, commissions et activit s hors cr dit. Ce ratio — stable et lev — traduit une d pendance structurelle au modèle de facturation de services, ind pendamment du cycle de taux directeurs. III. ANALYSE COMPARATIVE RÉGIONALE Le tableau ci-dessous consolide les indicateurs disponibles pour les huit march s de comparaison retenus. Les donn es NIR proviennent de la Banque Mondiale (GFDD.EI.03) ; les taux de bancarisation croisent les donn es BAM, FMI et Banque Mondiale 2024. Pays NIR / Total Bancarisation 2024 Frais transferts R gulation frais Maroc 40,3 % (2021) 58 % ~3–4 % (r form BAM) Mod r — socle GPBM 2006 + BAM actif Tunisie ~42–45 % (est.) ~45 % ~8 % ( lev ) Faible — peu contraignant Égypte En hausse ~37 % 5–7 % En renforcement post-2022 S n gal 35,7–42,5 % ~54 % (UEMOA) 3–5 % (BCEAO) Mod r — BCEAO harmonis Côte d'Ivoire ~48–55 % (est.) ~41 % 3–5 % (BCEAO) Mod r — même cadre BCEAO Kenya ~38–42 % ~79 % ~4–6 % Fort — CBK très actif Jordanie ~35–38 % ~43 % 4–6 % Mod r — CBJ encadre Afrique du Sud 40,9 % (2021) >80 % N/A (march mature) Fort — SARB + NCA Sources : World Bank GFDD/FRED, McKinsey African Banking 2026, BAM, BCT, BCEAO, CBK, estimations M3T Consulting. 3.1 Le Maroc en position interm diaire Avec 40,3 % de NIR sur total revenus, le Maroc se positionne dans le tier sup rieur de la r gion, au même niveau que l'Afrique du Sud (40,9 %), mais en dessous des march s UEMOA (Côte d'Ivoire, S n gal historique) où la part NIR peut atteindre 55 %. Par rapport à la Tunisie, le Maroc pr sente une meilleure r gulation des frais sur transferts — r sultat direct de l'action volontariste de Bank Al-Maghrib, qui a divis par deux ces frais, là où la Tunisie maintient un taux de 8 % d favorable aux expatri s. 3.2 Le modèle kenyan : r f rence en matière d'inclusion Le Kenya affiche un taux de bancarisation de ~79 % avec une part NIR similaire au Maroc (~38–42 %). Ce paradoxe apparent s'explique par la strat gie proactive de la Central Bank of Kenya (CBK) : l'exon ration temporaire des frais M-Pesa pendant la pand mie (2020–2021) a acc l r l'adoption digitale massive. La leçon : la r duction cibl e de frais sur un vecteur d'accès privil gi (mobile) peut produire un effet de bascule sur la bancarisation, ind pendamment du niveau global de NIR. 3.3 La zone UEMOA : niveau NIR lev , bancarisation faible La Côte d'Ivoire et le S n gal affichent historiquement les parts NIR les plus lev es de l' chantillon, dans des march s où la bancarisation reste inf rieure à 55 %. Ce constat illustre l'effet de segmentation : les frais lev s concentrent les revenus sur une clientèle captive (salari s du secteur formel, entreprises) tout en excluant les m nages à revenus irr guliers. IMPACT DES FRAIS SUR LE TAUX DE BANCARISATION 4.1 Les donn es macroscopiques (BAM 2024) Le taux de bancarisation au Maroc s' tablit à 58 % à fin 2024, contre 53 % stable de 2020 à 2022 — un plafonnement structurel sur trois ans malgr la dynamique d mographique. Cette stagnation est partiellement corr l e à la persistance de frais qui rigent un seuil d'entr e conomique pour les m nages à faible revenu. Taux de bancarisation 2024 Primo-bancaris s 2024 Comptes bancaires (total) 58 % (+4 pts vs 2023) 883 579 personnes 38,2 millions (+5,2 %) Hommes : 70 % | Femmes : 46 % 55 % hommes | 45 % femmes Recul ouvertures : -6,1 % Source : Bank Al-Maghrib — Statistiques bancaires 2024. ⚠ Signal d'alerte : le recul de -6,1 % du nombre total de comptes ouverts en 2024, malgr la hausse du nombre de primo-bancaris s, traduit une rationalisation des comptes multiples. Les Marocains ferment des comptes secondaires pour r duire leurs charges de tenue de compte — preuve directe de l'impact des frais sur les comportements bancaires. 4.2 Cartographie des obstacles li s aux frais Obstacle identifi M canisme d'impact Intensit (Maroc) Frais de tenue de compte Coût fixe mensuel dissuasif pour faibles revenus ●●●○○ Mod r e Frais de carte bancaire Repr sente 10–15 % du SMIG mensuel pour une carte Classic ●●●●○ Élev e Frais de virement hors place P nalise les zones rurales loign es d'agences ●●●●○ Élev e Commission de change Obstacle pour les MRE / travailleurs transfrontaliers ●●○○○ Faible (r form ) Frais interbancaires (CMI) Rench rit le paiement lectronique vs. cash ●●●○○ En baisse (2025) Complexit documentaire Frais implicites (temps, d placements, justificatifs) ●●●●● Très lev e M fiance institutionnelle Frein culturel amplifi par perception de frais injustifi s ●●●●○ Élev e Lecture : ●●●●● = obstacle très lev ; ○○○○○ = obstacle n gligeable. 4.3 Effets diff renci s par segment de population L'impact des frais sur la bancarisation n'est pas uniforme. Quatre segments sont particulièrement expos s : Segment Sp cificit de l'impact Indicateur de r f rence Femmes Frais de carte et tenue de compte repr sentent une part plus importante du revenu disponible (revenus moyens inf rieurs, emploi informel pr pond rant) Bancarisation femmes : 46 % vs 70 % hommes (2024) Zones rurales Frais de d placement implicites (accès agence) + frais de virement lev s. Le cash reste le mode dominant par d faut conomique. < 1 agence pour 10 000 habitants en zone rurale (BAM 2023) Jeunes 18–25 ans Primo-entrants sans revenus stables : coût annuel carte + tenue de compte (~400–500 MAD/an) constitue un frein à l'entr e 55 % des primo-bancaris s 2024 ont moins de 25 ans MRE / diaspora Frais de transferts impactent volume d'envois et recours aux canaux formels vs. informels R forme BAM : effet positif mesurable sur part du canal bancaire RÉFORMES EN COURS ET LEVIERS STRATÉGIQUES Consciente de ces freins, Bank Al-Maghrib a engag depuis 2019 une s rie de r formes cibl es dont l'efficacit commence à produire des effets mesurables. Elles s'articulent autour de quatre axes : 5.1 Strat gie Nationale d'Inclusion Financière — SNIF 2019–2027 La SNIF Phase 1 (2019–2023) a permis le renforcement du cadre l gal (loi sur les tablissements de paiement), le d veloppement des comptes de paiement simplifi s, et l' ducation financière. La Phase 2 (2024–2027) met explicitement l'accent sur la r duction des frais de transaction comme levier d'inclusion. Objectif d clar : atteindre 75 % de bancarisation à horizon 2027 Levier cl : comptes de paiement à coût minimal pour les populations à faible revenu Éducation financière : programme SNIF int grant la transparence des frais 5.2 Ouverture du march des paiements (2025) Fin 2024, le Conseil de la Concurrence a mis fin au quasi-monopole du Centre Mon tique Interbancaire (CMI), ouvrant le march marocain des paiements lectroniques à la concurrence effective dès le 1er mai 2025. BAM a parallèlement plafonn la commission interbancaire à 0,65 % de la valeur de la transaction. 5.3 Digital Morocco 2030 Le plan Digital Morocco 2030 (lanc septembre 2024) vise à faire du paiement mobile un pilier de la transformation num rique nationale. La digitalisation des paiements de l'État (protection sociale, allocations) r duit structurellement la d pendance au cash et cr e un point d'entr e bancaire pour des m nages auparavant exclus. 5.4 Benchmarks de bonnes pratiques r gionales Pays Mesure R sultat / Impact Kenya Exon ration temporaire frais M-Pesa (2020–2021, CBK) + compte M-Shwari à frais nuls Passage de ~50 % à ~79 % de bancarisation en 5 ans Rwanda Compte bancaire de base gratuit impos par la BNR à toutes les banques commerciales Bancarisation +30 pts en 7 ans (20 % → 50 %+) UEMOA Harmonisation BCEAO des plafonds de commissions sur transferts et mon tique Mobile money : 35–50 % des adultes en zone UEMOA Égypte Compte national (Meeza card) à frais minimaux — programme BCÉ 2022+ + 8 millions de nouveaux comptes en 2 ans RECOMMANDATIONS STRATÉGIQUES Sur la base de l'analyse comparative et des benchmarks identifi s, M3T Consulting formule les recommandations suivantes, articul es selon les trois niveaux d'action (r gulateur, secteur bancaire, État) : A — Niveau r gulateur (Bank Al-Maghrib / GPBM) Étendre le p rimètre des services gratuits : inclure les virements digitaux intrabanque et le relev lectronique dans le socle GPBM obligatoire Instaurer un Compte de Base Inclusif (CBI) : compte à tenue gratuite, carte de paiement à tarif social (< 60 MAD/an), virement lectronique inclus — à l'image du modèle rwandais Renforcer la transparence tarifaire : publication comparative trimestrielle BAM accessible en ligne et en agence Acc l rer la supervision des frais interbancaires post-CMI : suivi ex-post des effets de l'ouverture 2025 sur les tarifs r percut s aux consommateurs B — Niveau secteur bancaire ( tablissements) D velopper des offres segment es à tarification sociale : formules jeunes (< 25 ans) et femmes sans emploi avec tenue de compte gratuite pendant 24 mois Digitaliser la facturation : migration des op rations courantes vers le digital sans frais additionnels D ployer les agents bancaires en zones rurales : modèle d'agent banking r duisant les frais implicites de d placement Former les quipes front-office à l'explication des frais : r duire la m fiance par la transparence relationnelle C — Niveau État / politique publique Acc l rer la digitalisation des paiements sociaux (AMO, allocations, indemnit s) : cr e un ancrage bancaire obligatoire pour des millions de m nages non-bancaris s Conditionner l'accès aux march s publics et aux subventions à la domiciliation bancaire des TPE Inclure les frais bancaires dans l' ducation financière nationale : programmes ciblant les femmes rurales, les jeunes et les TPE VII. CONCLUSION Le Maroc occupe une position interm diaire dans le paysage bancaire r gional : ses frais hors int rêts sont significatifs (NIR ~40 % du total revenus) mais mieux r gul s que la Tunisie sur les transferts, comparables à l'Afrique du Sud sur la structure globale, et moins lev s que les march s UEMOA sur les commissions de services. Les frais bancaires constituent un frein r el et document à la bancarisation des segments vuln rables — femmes, zones rurales, jeunes sans revenus stables — et leur r duction cibl e repr sente l'un des leviers les plus directs disponibles pour franchir le seuil symbolique de 75 % fix par la SNIF. Les exp riences du Kenya, du Rwanda et de l'Égypte d montrent qu'un compte de base à coût minimal ou nul peut produire des effets d'inclusion massifs en quelques ann es. L'enjeu pour les banques marocaines est de r concilier deux imp ratifs : la rentabilit des revenus non-int rêts (indispensable à la solidit du secteur) et l'accessibilit tarifaire (n cessaire à l'approfondissement du march domestique). Ces deux objectifs ne sont pas contradictoires : un march bancaris à 75 % g nère structurellement plus de revenus qu'un march bloqu à 58 %. ◆ Conclusion analytique M3T : La r duction des frais bancaires hors int rêts n'est pas un sacrifice de rentabilit — c'est un investissement dans le march adressable. Les banques marocaines qui d velopperont les offres inclusives les plus comp titives captureront en premier les 11 millions d'adultes marocains encore non-bancaris s. C'est la logique du « profit through inclusion » qui transforme l'objectif r glementaire en opportunit strat gique. ANNEXE A — GLOSSAIRE DES TERMES TECHNIQUES Les termes ci-dessous sont d finis dans leur acception sp cifique au contexte de cette analyse. Ils sont list s par ordre alphab tique pour une consultation ais e. Terme D finition complète Bancarisation Taux de la population adulte disposant d'au moins un compte bancaire actif dans un tablissement de cr dit agr . Au Maroc, mesur et publi annuellement par Bank Al-Maghrib sur la base des donn es de la Centrale des comptes bancaires. Ne comprend pas les comptes de paiement mobile non rattach s à une banque. BCEAO (Banque Centrale des États de l'Afrique de l'Ouest) Institut d' mission commun des huit États membres de l'UEMOA (B nin, Burkina Faso, Côte d'Ivoire, Guin e-Bissau, Mali, Niger, S n gal, Togo). R gule et supervise les banques et tablissements financiers de la zone franc CFA, et harmonise la politique tarifaire sur les op rations bancaires transfrontalières. CMI (Centre Mon tique Interbancaire) Op rateur technique qui assurait jusqu'au 1er mai 2025 le quasi-monopole du traitement des paiements lectroniques interbancaires au Maroc (TPE, DAB, paiements en ligne). Sa position dominante a t remise en cause par le Conseil de la Concurrence fin 2024, ouvrant le march à de nouveaux entrants et à une comp tition sur les commissions d'interchange. Commission d'interchange Frais perçus par la banque mettrice de la carte bancaire auprès de la banque acqu reuse (celle du commerçant) lors de chaque transaction. Au Maroc, BAM a plafonn cette commission à 0,65 % de la valeur de la transaction en 2024, interdisant par ailleurs sa refacturation directe au consommateur final. FRED (Federal Reserve Economic Data) Base de donn es conomiques publique g r e par la Banque de R serve F d rale de St. Louis, qui h berge et diffuse l'ensemble des s ries statistiques du Global Financial Development Database (GFDD) de la Banque Mondiale. L'indicateur utilis dans cette analyse — GFDD.EI.03 — est accessible via les s ries DDEI03MAA156NWDB (Maroc) et quivalents pays. GFDD (Global Financial Development Database) Base de donn es produite par la Banque Mondiale mesurant le d veloppement financier de ~200 pays sur 4 dimensions : profondeur, accès, efficience et stabilit . L'indicateur GFDD.EI.03 mesure la part des revenus non-int rêts dans le total des revenus bancaires (NII + NIR), calcul à partir des donn es Bankscope sur donn es non consolid es. GPBM (Groupement Professionnel des Banques du Maroc) Organisation professionnelle f d rant l'ensemble des banques marocaines agr es. Interlocuteur de Bank Al-Maghrib pour la n gociation des conventions tarifaires, notamment l'accord de 2006 instituant la gratuit des services bancaires de base (ouverture de compte, ch quier, relev mensuel, versements d'espèces). Inclusion financière Accès de l'ensemble de la population — y compris les segments vuln rables (femmes, populations rurales, jeunes, TPE) — à des services financiers formels utiles et abordables : comptes de transaction, pargne, cr dit, paiement et assurance. Mesur e par la Banque Mondiale via l'indice Global Findex (enquête triennale). MRE (Marocains R sidant à l'Étranger) Diaspora marocaine tablie hors du Maroc, constituant un segment strat gique pour les banques marocaines (comptes devises, transferts de fonds). Les transferts MRE repr sentent environ 9–10 % du PIB marocain. La r forme des frais de transferts impuls e par BAM a directement b n fici à ce segment, r duisant le coût de rapatriement des fonds. NII (Net Interest Income) Revenu net d'int rêts : diff rentiel entre les produits g n r s par les cr dits accord s (int rêts perçus) et les charges pay es sur les d pôts collect s (int rêts vers s). Principal pilier de revenu des banques de d tail dans les march s mergents, compl mentaire au NIR. NIR (Non-Interest Revenue) Revenus bancaires hors int rêts, galement appel s revenus de commissions ou frais de services. Comprennent : commissions sur op rations (virements, chèques, cartes), frais de tenue de compte, revenus de change, gains sur trading et d riv s, produits sur services d'assurance et de banque de financement. Objet central de cette analyse. SNIF (Strat gie Nationale d'Inclusion Financière) Programme strat gique lanc en 2019 conjointement par Bank Al-Maghrib et le gouvernement marocain, structur en deux phases : Phase 1 (2019–2023) ax e sur le cadre l gal et les produits inclusifs ; Phase 2 (2024–2027) centr e sur la r duction des frais de transaction, l'infrastructure num rique et l' ducation financière. Objectif : porter le taux de bancarisation à 75 % d'ici 2027. TPE / TPME Très Petite Entreprise (TPE) et Très Petite et Moyenne Entreprise (TPME) : segment entrepreneurial prioritaire de la SNIF en matière d'accès au financement bancaire. Au Maroc, environ 88 % des PME restent sous-bancaris es selon les estimations sectorielles. Le programme Intelaka (6,8 Mds MAD distribu s en 2023) constitue le principal levier public de bancarisation de ce segment. UEMOA (Union Économique et Mon taire Ouest-Africaine) Zone d'int gration conomique et mon taire regroupant 8 pays d'Afrique de l'Ouest partageant le franc CFA BCEAO. Dispose d'un cadre r glementaire bancaire harmonis g r par la BCEAO, incluant des plafonds de commissions interbancaires et des règles de protection des consommateurs de services financiers. ANNEXE B — RÉFÉRENCES ET SOURCES AVEC LIENS ACTIFS RÉGULATEURS & BANQUES CENTRALES [1] Bank Al-Maghrib — Statistiques bancaires & comptes 2024 Donn es officielles sur le taux de bancarisation, nombre de comptes, primo-bancaris s 2024. [2] Bank Al-Maghrib — Rapports sur les infrastructures des march s financiers et moyens de paiement 2024 Strat gie nationale des paiements, cadre r glementaire CMI et paiements lectroniques. [3] Bank Al-Maghrib — Documents de travail de recherche 2024 Études conom triques sur les chocs de cr dit et la financiarisation de l' conomie marocaine. [4] Banque Centrale de Tunisie (BCT) — Tableau comparatif des frais bancaires Observatoire de l'Inclusion Financière de la BCT : comparatif tarifaire des banques tunisiennes. BANQUE MONDIALE & INSTITUTIONS MULTILATÉRALES [5] World Bank FRED — NIR/Total Income Maroc (DDEI03MAA156NWDB) S rie temporelle complète de l'indicateur GFDD.EI.03 pour le Maroc (2010–2021). [6] World Bank FRED — NIR/Total Income S n gal (DDEI03SNA156NWDB) Même indicateur pour le S n gal — base de comparaison UEMOA (2010–2020). [7] World Bank FRED — NIR/Total Income Afrique du Sud (DDEI03ZAA156NWDB) R f rence march mature africain (40,9 % en 2021). [8] FMI — Article IV Consultation Maroc 2024 (Staff Country Report 2024/099) Analyse macro conomique et bancaire, transmission des taux, croissance du cr dit 2023–2024. ÉTUDES & ANALYSES SECTORIELLES [9] McKinsey Global Institute — From Potential to Performance: A Snapshot of African Banking (mars 2026) Analyse des 5 march s leaders africains dont le Maroc. ROE, NIR vs NII, croissance 2024–2025. [10] MDPI Journal of Risk & Financial Management — Non-Interest Income in MENA Region Banks (mars 2024) Étude acad mique sur l'impact des revenus non-int rêts sur la rentabilit des banques MENA (40 banques, 2010–2022). [11] African Business — Africa's Top 100 Banks 2025 Classement et analyse des grandes banques africaines dont Attijariwafa Bank (3ème, Tier 1 capital 6,2 Mds $). PRESSE ÉCONOMIQUE & DONNÉES MAROC [12] M dias 24 — Taux de bancarisation 58 % au Maroc en 2024 (juillet 2025) Analyse d taill e de l' volution m thodologique et des donn es BAM 2024. [13] Le360 — Mobile et inclusion financière au Maroc (octobre 2025) SNIF, Digital Morocco 2030, fin du monopole CMI et enjeux de l'inclusion par le mobile. [14] LesEco.ma — Bancarisation : des progrès certains, mais des d fis persistants (juillet 2024) Analyse des freins structurels à la bancarisation dont l'impact des frais sur les populations vuln rables. [15] LesEco.ma — Bancarisation : l'objectif des 75 % se pr cise (juillet 2025) Donn es 2024, rationalisation des comptes multiples, tendances comportementales. [16] FNH.ma — Strat gie nationale d'inclusion financière : bilan 5 ans (novembre 2024) Bilan de la SNIF Phase 1 et objectifs de la Phase 2 (2024–2027). [17] Le Matin — Inclusion financière : Bank Al-Maghrib acc lère ses r formes (f vrier 2026) Interview BAM sur les priorit s r glementaires : infrastructure num rique, frais, TPE. [18] Le360 — Bank Al-Maghrib acc lère sa strat gie pour r duire la d pendance au cash (d cembre 2025) Strat gie nationale des paiements BAM 2024 : commission interbancaire plafonn e à 0,65 %. [19] HAC.ma — How to Navigate Morocco's Banking and Financial System (janvier 2026) Synthèse pratique des frais bancaires marocains (change, cartes, conditions d'ouverture). [20] Babnet.tn — Baisser les frais bancaires tunisiens sur transferts à 3 % (juillet 2025) Comparaison des frais sur transferts Tunisie (~8 %) vs Maroc, S n gal, Côte d'Ivoire. © M3T Consulting 2026 — Toute reproduction partielle ou totale soumise à autorisation pr alable crite. R f rence : M3T-GRC-2026-007 v2.

by Youness El Kandoussi | 2 months ago | 0 Comment(s) | 101 Share(s) | Tags :

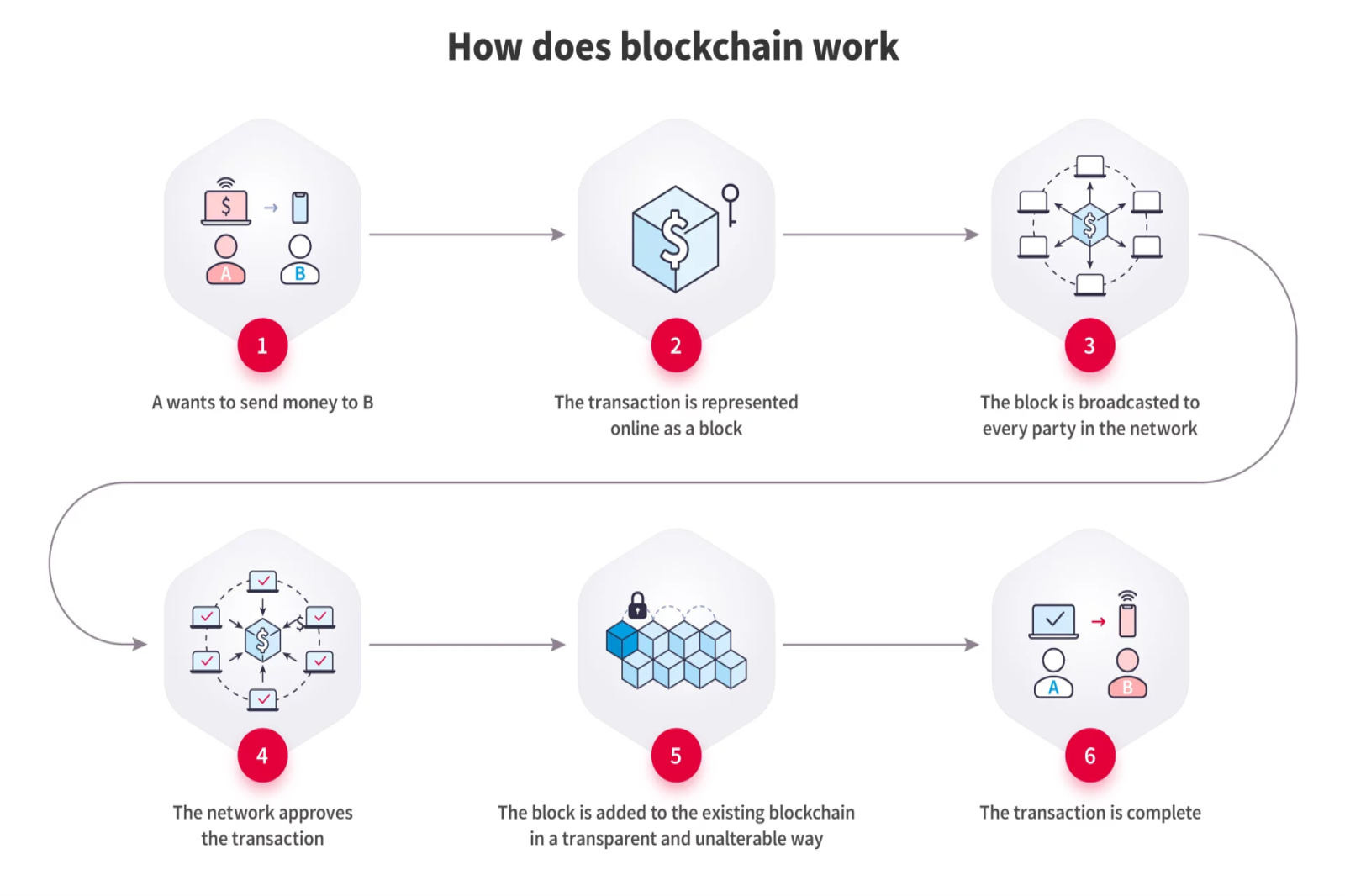

Table of Contents Introduction. 2 Definition and overview of blockchain technology. 2 Importance of blockchain in finance management. 2 Purpose of the presentation. 2 Understanding Blockchain. 2 Basics of blockchain technology. 2 Distributed ledger. 2 Decentralization. 3 Cryptography. 3 Key components of a blockchain. 3 Blocks. 3 Transactions. 3 Consensus mechanism.. 3 Different types of blockchains. 3 Public blockchains. 3 Private blockchains. 3 Consortium blockchains. 3 III. Implications of Blockchain in Finance Management. 3 Enhanced Security and Transparency. 3 Immutable records and tamper resistance. 3 Auditability and traceability. 3 Efficient and Cost-Effective Transactions. 4 Eliminating intermediaries. 4 Faster settlements and reduced transaction costs. 4 Smart Contracts and Automation. 4 Introduction to smart contracts. 4 Streamlined processes and reduced paperwork. 4 Fraud Prevention and Risk Mitigation. 4 Increased trust through consensus. 4 Improved identity verification and KYC processes. 4 Use Cases of Blockchain in Finance Management. 4 Cross-Border Payments and Remittances. 4 Supply Chain Finance. 4 Trade Finance and Letters of Credit. 4 Asset Tokenization and Securities Trading. 4 Peer-to-Peer Lending and Crowdfunding. 5 Insurance Claims and Underwriting. 5 Challenges and Considerations. 5 Scalability and performance issues. 5 Regulatory and legal concerns. 5 Interoperability between different blockchains. 5 Privacy and data protection. 5 Future Outlook. 5 Emerging trends and developments. 5 Collaboration between traditional finance and blockchain. 5 Potential impact on financial institutions and intermediaries. 5 VII. Conclusion. 5 Recap of key points. 5 Summary of blockchain's implications on finance management. 6 Potential benefits and opportunities. 6 Closing remarks. 6 I. Introduction A. Definition and overview of blockchain technology Blockchain technology is a decentralized and distributed ledger that records transactions across multiple computers. It enables secure and transparent transactions without the need for intermediaries. B. Importance of blockchain in finance management Blockchain has significant implications for finance management. It enhances security, reduces costs, automates processes, and mitigates fraud risks, transforming the way financial transactions are conducted. C. Purpose of the presentation The purpose of this presentation is to provide an understanding of blockchain technology and its implications in finance management. We will explore the key components of blockchain, its benefits, and various use cases in the financial industry. II. Understanding Blockchain A. Basics of blockchain technology 1. Distributed ledger Blockchain utilizes a distributed ledger, where multiple participants maintain and validate the transaction records collectively. This eliminates the need for a central authority and enhances trust. 2. Decentralization Blockchain operates in a decentralized manner, meaning no single entity has control over the entire network. This ensures transparency, resilience, and reduces the risk of a single point of failure. 3. Cryptography Blockchain uses cryptographic techniques to secure transactions and ensure data integrity. It employs cryptographic hash functions and digital signatures to authenticate and protect the information stored on the blockchain. B. Key components of a blockchain 1. Blocks Blocks are the building blocks of a blockchain and contain a set of transactions. Each block is linked to the previous block through a cryptographic hash, forming a chain of blocks. 2. Transactions Transactions represent the exchange of assets or information on the blockchain. They are recorded in blocks and are typically validated by network participants through a consensus mechanism. 3. Consensus mechanism Consensus mechanisms ensure agreement among network participants on the validity of transactions. It enables trust and prevents fraudulent activities. Common consensus mechanisms include Proof of Work (PoW), Proof of Stake (PoS), and Practical Byzantine Fault Tolerance (PBFT). C. Different types of blockchains 1. Public blockchains Public blockchains are open and accessible to anyone. They are maintained by a decentralized network of participants, and anyone can join the network, validate transactions, and create blocks. Bitcoin and Ethereum are examples of public blockchains. 2. Private blockchains Private blockchains are restricted to a specific group of participants. They provide privacy and control over the network, making them suitable for enterprises and organizations. Access to the blockchain is permissioned, and participants are often known entities. 3. Consortium blockchains Consortium blockchains are a hybrid between public and private blockchains. They are operated and maintained by a consortium or a group of organizations that have shared control over the network. Consortium blockchains offer a balance between openness and control. III. Implications of Blockchain in Finance Management A. Enhanced Security and Transparency 1. Immutable records and tamper resistance Blockchain's immutability ensures that once a transaction is recorded on the blockchain, it cannot be altered or deleted. This provides a high level of security and reduces the risk of fraud and tampering. 2. Auditability and traceability Blockchain's transparent nature enables easy auditing of transactions. Each transaction is recorded on the blockchain, creating an auditable trail of activities. This enhances transparency and accountability in financial transactions. B. Efficient and Cost-Effective Transactions 1. Eliminating intermediaries Blockchain eliminates the need for intermediaries, such as banks or clearinghouses, in financial transactions. This reduces costs, speeds up processes, and enables direct peer-to-peer transactions. 2. Faster settlements and reduced transaction costs Blockchain enables near-instantaneous settlements compared to traditional systems that may take days. It also reduces transaction costs by removing intermediaries and streamlining processes. C. Smart Contracts and Automation 1. Introduction to smart contracts Smart contracts are 2. Streamlined processes and reduced paperwork Smart contracts automate and streamline various financial processes, eliminating the need for manual paperwork and reducing human errors. This increases efficiency and accelerates transaction processing. D. Fraud Prevention and Risk Mitigation 1. Increased trust through consensus Blockchain's consensus mechanisms foster trust and prevent fraudulent activities. The distributed nature of blockchain ensures that transactions are verified by multiple participants, reducing the risk of fraud or manipulation. 2. Improved identity verification and KYC processes Blockchain technology can enhance identity verification and Know Your Customer (KYC) processes. It allows for secure storage and sharing of verified user data, reducing the risk of identity theft and fraud. IV. Use Cases of Blockchain in Finance Management A. Cross-Border Payments and Remittances Blockchain facilitates faster and cheaper cross-border payments by eliminating intermediaries, reducing fees, and providing real-time transaction tracking. B. Supply Chain Finance Blockchain enhances supply chain finance by enabling transparent and secure tracking of goods, verifying authenticity, reducing fraud, and streamlining payment processes. C. Trade Finance and Letters of Credit Blockchain simplifies trade finance by digitizing and automating the processing of letters of credit, reducing paperwork, and improving trust among participants. D. Asset Tokenization and Securities Trading Blockchain enables the tokenization of assets such as real estate or artwork, making them divisible and tradable. It enhances liquidity, simplifies ownership transfer, and reduces intermediaries in securities trading. E. Peer-to-Peer Lending and Crowdfunding Blockchain platforms facilitate peer-to-peer lending and crowdfunding by connecting borrowers directly with lenders, automating loan agreements, and providing transparency and auditability. F. Insurance Claims and Underwriting Blockchain streamlines insurance processes by automating claims processing, reducing fraud through transparent records, and improving underwriting accuracy through access to verified data. V. Challenges and Considerations A. Scalability and performance issues Blockchain faces challenges in scaling to accommodate a large number of transactions and maintaining performance. Solutions like layer-two protocols and sharding are being explored to address these challenges. B. Regulatory and legal concerns Blockchain's decentralized nature raises regulatory and legal concerns, such as data privacy, cross-border transactions, and compliance with existing financial regulations. Regulatory frameworks need to evolve to address these issues. C. Interoperability between different blockchains Interoperability between different blockchains is essential for seamless integration and exchange of assets and information. Efforts are underway to develop standards and protocols for interoperability. D. Privacy and data protection While blockchain provides transparency, preserving privacy and protecting sensitive data is crucial. Privacy-enhancing technologies like zero-knowledge proofs and secure multiparty computation are being developed to address these concerns. VI. Future Outlook A. Emerging trends and developments Emerging trends include the integration of blockchain with other technologies like artificial intelligence, Internet of Things, and decentralized finance (DeFi). These developments have the potential to revolutionize finance management further. B. Collaboration between traditional finance and blockchain Traditional financial institutions are exploring blockchain technology and collaborating with blockchain startups to leverage its benefits. Partnerships and consortia are being formed to drive innovation and adoption in the financial industry. C. Potential impact on financial institutions and intermediaries Blockchain has the potential to disrupt traditional financial institutions and intermediaries. They will need to adapt and innovate to remain competitive in a decentralized and digitally transformed financial landscape. VII. Conclusion A. Recap of key points Blockchain technology is a decentralized and transparent ledger that offers enhanced security, efficiency, automation, and fraud prevention in finance management. B. Summary of blockchain's implications on finance management Blockchain technology improves security, reduces costs, stream C. Potential benefits and opportunities Implementing blockchain in finance management can lead to reduced transaction costs, faster settlements, improved fraud prevention, and increased efficiency and transparency, unlocking new opportunities for innovation and growth. D. Closing remarks Blockchain technology has the potential to reshape the finance industry by revolutionizing how transactions are conducted, recorded, and verified. Embracing blockchain's capabilities can drive a more secure, efficient, and inclusive financial ecosystem.

by Youness El Kandoussi | 3 years ago | 0 Comment(s) | 1567 Share(s) | Tags :

POST COMMENT

COMMENTS(0)

No Comment yet. Be the first :)