ABOUT AUTHOR

Youness EL Kandoussi is a seasoned Consultant Risk Expert with over 23 years of experience in Operational Risk Management, Islamic Finance, and Professional Training. He holds a certification as an Operational Risk Expert from the London School of Business & Finance (2018). Throughout his career, Youness has successfully led numerous large-scale projects for various banks, from conception to completion, ensuring their success in terms of costs and timelines. He has also been actively involved in conducting training programs on Risk Management for executives and employees of Financial Institutions, Public Administrations, Cooperatives, and Associations. Accomplishments Youness EL Kandoussi's notable accomplishments include: • Conducting successful certified training programs in Risk Management for professionals across different sectors. • Moderating and participating in various seminars and conferences within the financial industry and FinTech. • Implementing Operational Risk Management Systems and Risk Mapping for prominent institutions like SGMA, CDG Invest, and Umnia Bank. • Leading the implementation of Operational Risk Management Systems and Reporting projects, including functional specifications development and System implementation.

CATEGORIES

READ ALSO

Contents 1 Abstract.. 4 2 Introduction.. 4 3 Objective: 5 4 Plan of the paper: 5 5 Chapter 1: Risk History and definitions. 5 5.1 Introduction: 5 5.2 Section I: Risk Management History: 6 5.3 Section 2: Definitions of Risk Management: 7 5.3.1 Market Risk: 8 5.3.2 Credit Risk. 8 5.3.3 Liquidity Risk: 8 5.3.4 Operational Risk: 9 6 Chapter 2: Evolvement of Risk Management: Basel I, II and III. 10 6.1 Introduction: 10 6.2 Section I: Basel I and its shortcomings: 11 6.3 Section 2: Basel II 12 6.4 Section 3: Basel III 13 6.4.1 Summary OF changes. 13 7 Chapter 3: Risk in Islamic Finance Institutions. 14 7.1 Introduction: 14 7.2 Section 1: Islamic Finance Institutions are unique. 16 7.3 Section 2: Types of Risks in the IFIs: 17 8 Chapter 4: Islamic Finance Products, Risks and the key challenges. 19 8.1 Introduction: 19 8.2 Section 1: Risks in Islamic Finance Products: 19 8.2.1 Risks in Musharakah Contracts: 21 8.2.2 Risks in Mudarabah contract: 22 8.2.3 Risks in Murabahah Contract: 24 8.2.4 Risks in Salam Contract: 24 8.2.5 Risks in Istisnaa Contract 25 8.2.6 Risks in Iajrah Contract: 26 8.3 Section 2: Challenges of Risk Management in Islamic Finance Products. 27 9 Chapter 5: Operational Risk in Islamic Finance Institutions. 28 9.1 Introduction: 28 9.2 Section 1: Operational Risk in Musharakah contract: 28 9.3 Section 2: Operational Risk in Mudarabah contract. 29 9.4 Section 3: Operational Risk in Murabahah contract. 29 9.5 Operational Risk in Salam contract. 30 9.6 Operational Risk in Istisnaa contract: 30 9.7 Operational Risk in Ijarah contract: 30 10 Conclusion.. 30 10.1 Findings. 30 10.2 Recommendations. 31 11 References. 33 1 Abstract As IFIs are growing extensively and expected to grow up to 15% in the coming years, it is primordial that all the industry stakeholders start to invest their efforts to develop the Risk Management disciplines. The IFSB and AAOIFI are not sparing any effort to guide and participate in shaping the IF Risk Management, however, they tend to be inspired by the existing frameworks historically developed for Conventional Banks. Islamic Finance contracts are very different in nature and in substance from conventional banks, thus, the conventional Risk Management cannot cater for their uniqueness. This paper tried to highlight uniqueness of risk aspects within the IF contracts, and focused on Operational Risk, which is in my opinion in the major risk for IFI. 2 Introduction Risk Management have evolved since its first appearance after the World War II. The Bank of International Settlement have tried to adapt to the changes in the Finance industry and issued 3 version of the Basel Guidelines on Capital Requirements (Basel I, II and III). These guidelines have identified Capital Requirements for Credit Risk, Market Risk and Operational Risk. They also issued Sound Practices for Risk Management for each type of Risk. With the venue of the Islamic Finance Industry in the 1960s, Risk Management tools had to adapt to the uniqueness of their products. IFSB and AOIIFI have invested huge efforts in developing Risk Management guidelines for IFIs. Scholars and Islamic Finance practitioners issued multitude of papers attempting to circle aspects of Risk in the Islamic Finance Contracts. They have demonstrated that Islamic Finance encompasses other types of Risk that are unknown to conventional Banks (Fiduciary Risk, Sharia non-compliance Risk, Commercial Displaced Risk, etc.) Many of those scholars have also found out that the IFIs are more exposed to Operational Risk than the conventional banks, mainly due to the complexity of the contracts and their execution. This research is an attempt to add some more light on Risks faced by Islamic Finance Institution with a special focus on Operational Risk. 3 Objective: Risk Management in IFIs tends to be complex and least understood by the business and even by the Risk Management practitioners, in this research I will attempt to define Risks in IFIs and clarify its specifications by demonstrating its uniqueness, especially in the Islamic Finance contracts, where each contract can encompass more than one type of Risk. I will also try to cover some more details of Operational Risk aspects in the IF contracts and demonstrate its importance and complexity during the lifecycle. That being discussed I will propose some actions that can enhance the Operational Risk Management within the IFIs. 4 Plan of the paper: In this paper, I will be defining Risk Management in general in Financial Institutions and its degree of evolvement especially in conventional banking, how Risk is different in Islamic Financial Institutions from conventional banks, their instruments and what are the key challenges. Then I will be discussing the Operational Risk Management in Islamic Finance Institutions and its specifications. 5 Chapter 1: Risk History and definitions 5.1 Introduction: Risk Management emerged after the World War II, and began to be studied in universities as a discipline with the two academic books ( Mehr and Hedges (1963) and Williams and Hems (1964)[1]. Risk Management was, for a long time, the ultimate tool for Insurance Industry aiming to mitigate Risks related to individuals and companies from losses incurred from accidents[2] After 1950s, and due to the increasing costs of insurance, various Risk Management activities were introduced to the business (e.g. business continuity, self-insurance). Derivatives were introduced after 1970s to mitigate the faced risks. Market, Credit, and Operational Risk Management tools were introduced to manage the emerging risks from the intensified activities with insurance and Finance industries (consequently after 1980s for Market and Credit and 1990s for Operational Risk)[3] The objective of a financial institution (or for any kind of business) is to maximize shareholders’ profits by adding value and best usage of available resources. Financial institutions, in particular, have to manage Risks to achieve the aforesaid objective. Risk is defined as a possible adverse, one or more, outcomes, it is unknown for its intrinsic volatility and unpredictability. Financial institutions face different types of Risks. Business Risks, which “arises from the nature of a firm’s business. It relates to factors affecting the product market. Financial risk arises from possible losses in financial markets due to movements in financial variables [4]”. Oldfield and Santomero classifies Risk in three types: risks that can be eliminated, those that can be transferred to others, and the risks that can be managed by the institution. [5]” Besides the above given definitions, Risk can also be defined as Financial Risk, i.e. Credit Risk and Market Risk, and non-Financial Risk, i.e., among others, Operational Risk, Legal Risk, Reputational Risk and Strategic Risk.[6] 5.2 Section I: Risk Management History: Risk Management historically was the main objective of the insurance industry. After the World War II, large companies started to mitigate their risks by introducing Self-Insurance techniques. It was largely applied to cover adverse financial impacts consequent of events of losses or Market volatility. After 1970s, Financial Risk Management emerges as a cornerstone for multitude of companies including banks. In Fact, Stock Market prices, exchange rates, commodity prices, were their main concerns. Table 1: Milestones in the History of Risk Management[7] In 1990s Risk Management took more momentum and became a high priority matter for corporates, Board of Director have now the responsibility of oversight and monitoring policies effected by the Board Audit and Risk Management Committees. Financial Institution, after 2000s are required to implement capital reserves for risks, especially after the major defaults and the Enron bankruptcy case. Basel II (2004) issued guidelines on more robust capital requirements on banks for Credit Risk, also introduced rules on managing Operational Risk. In 2010 Basel III came as a response to the 2008 subprime crisis, with more constraints on capital requirements and new Liquidity Risk Management guidelines. 5.3 Section 2: Definitions of Risk Management: According to Wikipedia, “Risk management is the identification, assessment, and prioritization of risks (defined in ISO 31000 as the effect of uncertainty on objectives) followed by coordinated and economical application of resources to minimize, monitor, and control the probability and/or impact of unfortunate events[8] or to maximize the realization of opportunities. Risk management’s objective is to assure uncertainty does not deflect the endeavor from the business goals.[9]” Financial Institutions face generally two types of Risk, Financial and Non-Financial[10] (Gleason 2000). Financial Risks are those due Market volatility (Market Risk), and those due customers’ defaults (Credit Risk). Non-Financial Risk includes, but not limited to, Operational Risk, Legal Risk, Reputational Risk, Regulatory Compliance Risk. 5.3.1 Market Risk: Market Risk is defined as the risk from adverse volatility of traded instruments and assets in a well-defined Market[11]. Market Risk can affect both banking and trading books. In the sense that it is originated from equity price risk, interest rate risk, currency risk, and commodity price risk. Market Risk is said systematic when it arises due to the general volatility of prices and overall changes in policies in the economy. When the price of a specific asset or instruments changes due to events inherent to it, it is categorized as unsystematic Risk. 5.3.2 Credit Risk “Credit risk is most simply defined as the potential that a bank borrower or counterparty will fail to meet its obligations in accordance with agreed terms. The goal of credit risk management is to maximize a bank's risk-adjusted rate of return by maintaining credit risk exposure within acceptable parameters. Banks need to manage the credit risk inherent in the entire portfolio as well as the risk in individual credits or transactions. Banks should also consider the relationships between credit risk and other risks. The effective management of credit risk is a critical component of a comprehensive approach to risk management and essential to the long-term success of any banking organization.”[12] Credit Risk is the risk that counterparty will fail to meet its obligations timely and fully in accordance with the agreed terms[13]. 5.3.3 Liquidity Risk: The Principles for Sound Liquidity Risk Management and Supervision[14] (BCBS 2008) defines Liquidity as “the ability of a bank to fund increases in assets and meet obligations as they come due, without incurring unacceptable losses.” Liquidity Risk arises then from adverse circumstances that hurdles a bank to normally operate and meet its liabilities when due. Funding Liquidity Risk occurs when banks are unable to secure funds at a reasonable cost from borrowing, Asset Liquidity Risk arises when banks face difficulties to generate liquidity from sale of assets.[15] 5.3.4 Operational Risk: The BCBS Principles for the Sound Management of Operational Risk defines Operational Risk as the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. This definition includes legal risk, but excludes strategic and reputational risk.[16] Operational Risk was for a long time out of the radar of the corporates and scholars, it was not quite understood. Power writes: “Operational risk was conceived as a composite term for a wide variety of organizational and behavioural risk issues which were traditionally excluded from formal definitions of market and credit risk. The explosion of operational risk discourse gave new structure and rationality to what had traditionally been regarded as a risk management residual and negatively described as non-financial risk.”[17] The Bank of international Settlements (BIS) have categorized Operational Risk into four causal categories[18]: · Process · Business Process (lack of proper due diligence, inadequate/problematic account reconciliation, etc.) · Business Risks (merger risk, new product risk, etc.) · Errors and Omissions (inadequate/problematic security, inadequate/problematic quality control, etc.) · Specific Liabilities (employee benefits, employer, directors and officers, etc.) · People · Employee Errors (general transaction errors, incorrect routing of transaction, etc.) · Human Resource Issues (employee unavailability, hiring/firing, etc.) · Personal Injury – Physical Injury (bodily injury, health and safety, etc.) Personal Injury – Non–Physical Injury (libel/defamation/slander, discrimination/harassment, etc.) · Wrongful Acts (fraud, trading misdeeds, etc.) · Information Technology · General Technology Problems (operational error – technology related, unauthorized use/misuse of technology, etc.) · Hardware (equipment failure, inadequate/unavailable hardware, etc.) · Security (hacking, firewall failure, external disruption, etc.) · Software (computer virus, programming bug, etc.) · Systems (system failures, system maintenance, etc.) · Telecommunications (telephone, fax, etc.) · External Events · Disasters (natural disasters, non–natural disasters, etc.) · External Misdeeds (external fraud, external money laundering, etc.) · Litigation/Regulation (capital control, regulatory change, legal change, etc.) · Relationships · Legal/Contractual (securities law violations, legal liabilities, etc.) · Negligence (gross negligence, general negligence, etc.) · Sales Discrimination (lending discrimination, client Discrimination, etc.) · Sales Related Issues (churning, sales misrepresentation, high pressure sales tactics, etc.) · Specific Omissions (failure to pay proper fees, failure to file proper report, etc.) Gene Alvares attempted a mapping exercise between the Causal Categories and Basel Risk Types (Alvares, Global Association of Risk Professionals GARP studies. 2002). Mapping illustration between the Basel Committee’s proposed operational risk event classification scheme and Zurich IC2 format. (Alvarez, 2002)[19] References Georges Dionne, Risk Management: History and Critique, March 2013 Harrington and Neihaus, 2013, Georges Dionne, Risk Management: History and Critique, March 2013 Jorion and Khoury 1996, reference cited by Tariqullah Khan Habib Ahmed: Risk Management: An Analysis Of Issues In Islamic Financial Industry, 2001, Islamic Development Bank, Islamic Research and Training Institute Oldfield and Santomero (1997), reference cited by Tariqullah Khan Habib Ahmed: Risk Management: An Analysis Of Issues In Islamic Financial Industry, 2001, , Islamic Development Bank, Islamic Research and Training Institute Tariqullah Khan Habib Ahmed: Risk Management: An Analysis Of Issues In Islamic Financial Industry, 2001, Islamic Development Bank, Islamic Research and Training Institute Hubbard, Douglas (2009). The Failure of Risk Management: Why It's Broken and How to Fix It. John Wiley & Sons. (Wikipedia) Antunes, Ricardo; Gonzalez, Vicente (3 March 2015). "A Production Model for Construction: A Theoretical Framework". Buildings. 5 (1): 209–228. doi:10.3390/buildings5010209. (Wikipedia) BCBS - Principles for the Management of Credit Risk - final document, September 2000 BCBS - Principles for Sound Liquidity Risk Management and Supervision - final document, September 2008 BCBS Principles for the Sound Management of Operational Risk, 2011 Power p. 103 Cited by Johannes Gaus aus Böblingen, The Risks of Financial Risk Management, Master-Thesis, Economics of Financial Institutions European Business School, Department Corporate Management & Economics, Zeppelin University Marinoiu Ana Maria, Bucharest University of Economics, Faculty of International Business and Economics, Operational Risk In International Business: Taxonomy And Assessment Methods, Federal Reserve Bulletin, September 2003, Capital Standards for Banks: The Evolving Basel Accord BCBS, Basel II: The New Basel Capital Accord - third consultative paper April 2003 and Revised international capital framework, June 2006 Basel III: international regulatory framework for banks Sean Kenny, To What Extent were the Limitations of the Previous Basel Accords (I & II) overlooked by Basel III?, Master programme in Economic History, Lund University, School of Economics and Management, June 2011 BCBS- Pillar 2 (Supervisory Review Process), the New Basel Capital Accord, Principal 2 Basel II, Tamer Bakiciol Nicolas Cojocaru-Durand DongxuLu, December 2008 BIS, BCSB, Basel III: international regulatory framework for banks Basel Committee on Banking Supervision, Basel III: International Framework for Liquidity Risk Measurement, Standards and Monitoring, Dec 10, Bank for International Settlements. http://wwww.basel-ii-risk.com/basel-iii-guide-to-the-changes/ Ahmad Alharbi, Development of the Islamic Banking System, Journal of Islamic Banking and Finance June 2015, Vol. 3, No. 1 Syed Ehsan Ullah Agha, RISK MANAGEMENT IN ISLAMIC FINANCE: AN ANALYSIS FROM OBJECTIVES OF SHARI’AH PERSPECTIVE, International Journal of Business, Economics and Law, Vol. 7, Issue 3 (Aug.) 2015 Specifics of Risk Management in Islamic Finance and Banking, with Emphasis on Bosnia and Herzegovina, E.Kozarević, M.Baraković Nurikić & N.Nuhanović, Bahar/Spring 2014, Volume 4, Issue 1, Çankırı Karatekin University, Journal of The Faculty of Economics, and Administrative Sciences. Ioannis Akkizidis and Sunil Kumar Khandelwal, Financial Risk Management for Islamic Banking and Finance, Palgrave Macmillan. Standing Committee for Economic and Commercial Cooperation of the Organization of Islamic Cooperation (COMCEC), Risk Management in Islamic Financial Instruments, COMCEC Coordination Office, September 2014. ISLAMIC FINANCIAL SERVICES BOARD, GUIDING PRINCIPLES OF RISK MANAGEMENT FOR INSTITUTIONS (OTHER THAN INSURANCE INSTITUTIONS) OFFERING ONLY ISLAMIC FINANCIAL SERVICES, December 2005. Nurhafiza Abdul Kader Malim PhD, Islamic Banking and Risk Management: Issues and Challenges, Journal of Islamic Banking and Finance Oct.- Dec. 2015. Hennie van Greuning Zamir Iqbal, Risk Analysis for Islamic Banks, THE WORLD BANK Washington, D.C., December 2008. Ahmad Mohamed Rahim, Operational Risks in Islamic Profit Sharing Contracts and Ways to Overcome Them, MSc in Islamic Finance, The Global University of Islamic Finance, October 2014 (http://www.inceif.org/research-bulletin/operational-risks-islamic-profit-sharing-contracts-ways-overcome/) [1] Georges Dionne, Risk Management: History and Critique, March 2013, p. 1 [2] Harrington and Neihaus, 2013, Georges Dionne, Risk Management: History and Critique, March 2013, p. 1 [3] Georges Dionne, Risk Management: History and Critique, March 2013, p. 1 [4] Jorion and Khoury 1996, p. 2, reference cited by Tariqullah Khan Habib Ahmed: Risk Management: An Analysis Of Issues In Islamic Financial Industry, 2001,p. 26, Islamic Development Bank, Islamic Research and Training Institute [5] Oldfield and Santomero (1997), reference cited by Tariqullah Khan Habib Ahmed: Risk Management: An Analysis Of Issues In Islamic Financial Industry, 2001,p. 27, Islamic Development Bank, Islamic Research and Training Institute [6] Tariqullah Khan Habib Ahmed: Risk Management: An Analysis Of Issues In Islamic Financial Industry, 2001,p. 28, Islamic Development Bank, Islamic Research and Training Institute [7] Georges Dionne, Risk Management: History and Critique, March 2013, p. 6 [8] Hubbard, Douglas (2009). The Failure of Risk Management: Why It's Broken and How to Fix It. John Wiley & Sons. p. 46. (Wikipedia) [9] Antunes, Ricardo; Gonzalez, Vicente (3 March 2015). "A Production Model for Construction: A Theoretical Framework". Buildings. 5 (1): 209–228. doi:10.3390/buildings5010209. (Wikipedia) [10] Tariqullah Khan Habib Ahmed: Risk Management: An Analysis of Issues in Islamic Financial Industry, 2001, p. 28, Islamic Development Bank, Islamic Research and Training Institute [11] Tariqullah Khan Habib Ahmed: Risk Management: An Analysis of Issues in Islamic Financial Industry, 2001, p. 28, Islamic Development Bank, Islamic Research and Training Institute [12] BCBS - Principles for the Management of Credit Risk - final document, September 2000 [13] Tariqullah Khan Habib Ahmed: Risk Management: An Analysis of Issues in Islamic Financial Industry, 2001, p. 29, Islamic Development Bank, Islamic Research and Training Institute [14] BCBS - Principles for Sound Liquidity Risk Management and Supervision - final document, September 2008 [15] Tariqullah Khan Habib Ahmed: Risk Management: An Analysis of Issues in Islamic Financial Industry, 2001, p. 29, Islamic Development Bank, Islamic Research and Training Institute [16] BCBS Principles for the Sound Management of Operational Risk, 2011, p. 3 [17] Power p. 103 Cited by Johannes Gaus aus Böblingen, The Risks of Financial Risk Management, Master-Thesis, Economics of Financial Institutions European Business School, Department Corporate Management & Economics, Zeppelin University, p. 38 [18] Marinoiu Ana Maria, Bucharest University of Economics, Faculty of International Business and Economics, Operational Risk In International Business: Taxonomy And Assessment Methods, P. 196 [19] Marinoiu Ana Maria, Bucharest University of Economics, Faculty of International Business and Economics, Operational Risk in International Business: Taxonomy and Assessment Methods, P. 197

by Youness El Kandoussi | 3 years ago | 0 Comment(s) | 1465 Share(s) | Tags :

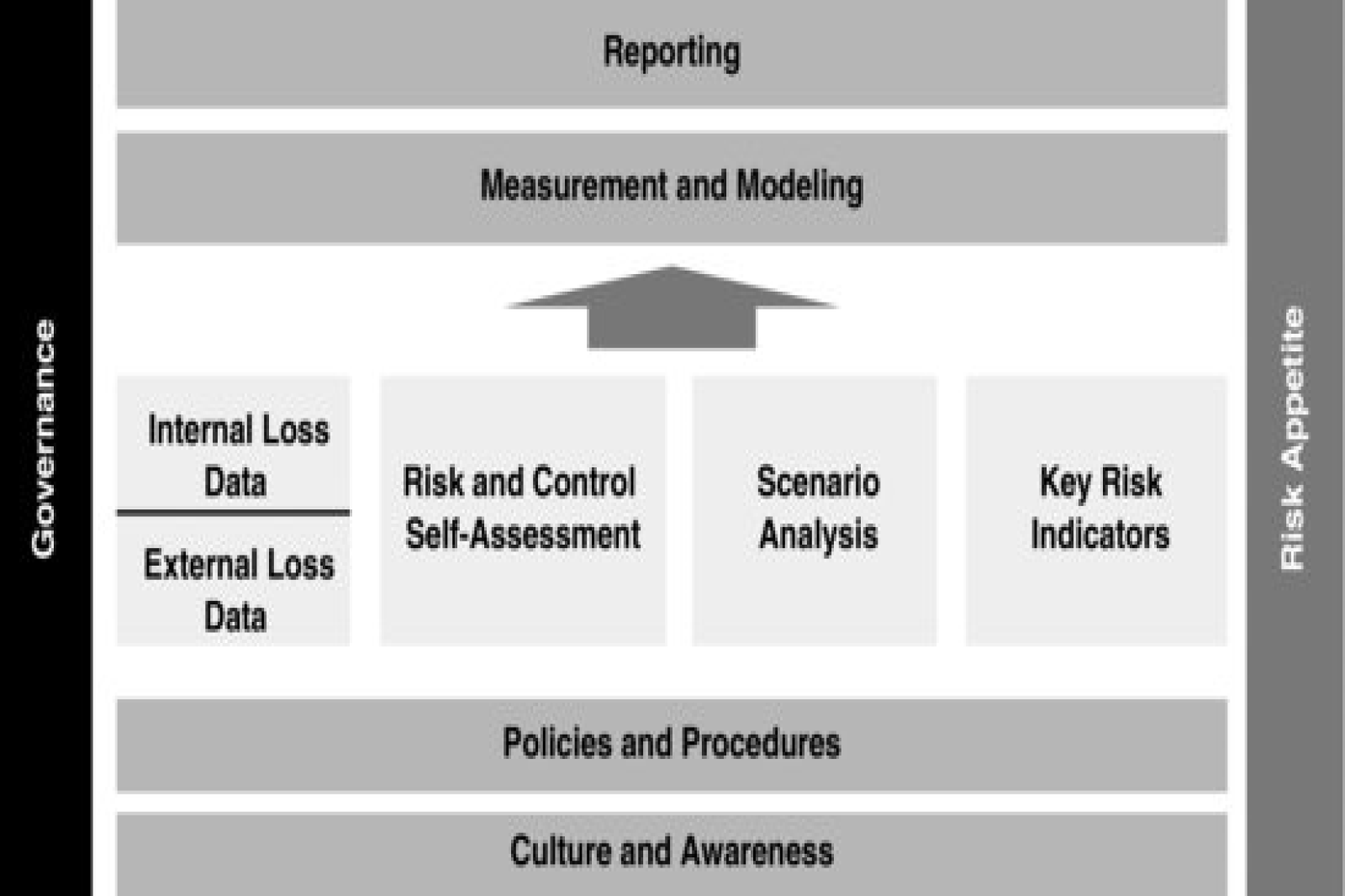

Operational Risk Governance:Sound Practices for the Management and Supervision of Operational Risk BIS June 2011 The Board of Directors Principle 3: The board of directors should establish, approve and periodically review the Framework. The board of directors should oversee senior management to ensure that the policies, processes and systems are implemented effectively at all decision levels. Principle 4: The board of directors should approve and review a risk appetite and tolerance statement for operational risk that articulates the nature, types, and levels of operational risk that the bank is willing to assume. Senior Management Principle 5: Senior management should develop for approval by the board of directors a clear, effective and robust governance structure with well defined, transparent and consistent lines of responsibility. Senior management is responsible for consistently implementing and maintaining throughout the organisation policies, processes and systems for managing operational risk in all of the bank’s material products, services and activities, consistent with the risk appetite and tolerance. Risk Management Environment Identification and Assessment Principle 6: Senior management should ensure the identification and assessment of the operational risk inherent in all material products, activities, processes and systems to ensure the inherent risks and incentives are well understood. Principle 7: Senior management should ensure that there is an approval process for all new products, activities, processes and systems that fully assesses operational risk. Monitoring and Reporting Principle 8: Senior management should implement a process to regularly monitor operational risk profiles and material exposures to losses. Appropriate reporting mechanisms should be in place at the board, senior management, and business line levels that support proactive management of operational risk. Control and Mitigation Principle 9: Banks should have a strong control environment that utilises: policies, processes and systems; appropriate internal controls; and appropriate risk mitigation and/or transfer strategies. Business Resiliency and Continuity Principle 10: Banks should have business resiliency and continuity plans in place to ensure an ability to operate on an ongoing basis and limit losses in the event of severe business disruption. Role of Disclosure Principle 11: A bank’s public disclosures should allow market participants to assess its approach to operational risk management.

by Youness El Kandoussi | 3 years ago | 0 Comment(s) | 1194 Share(s) | Tags :

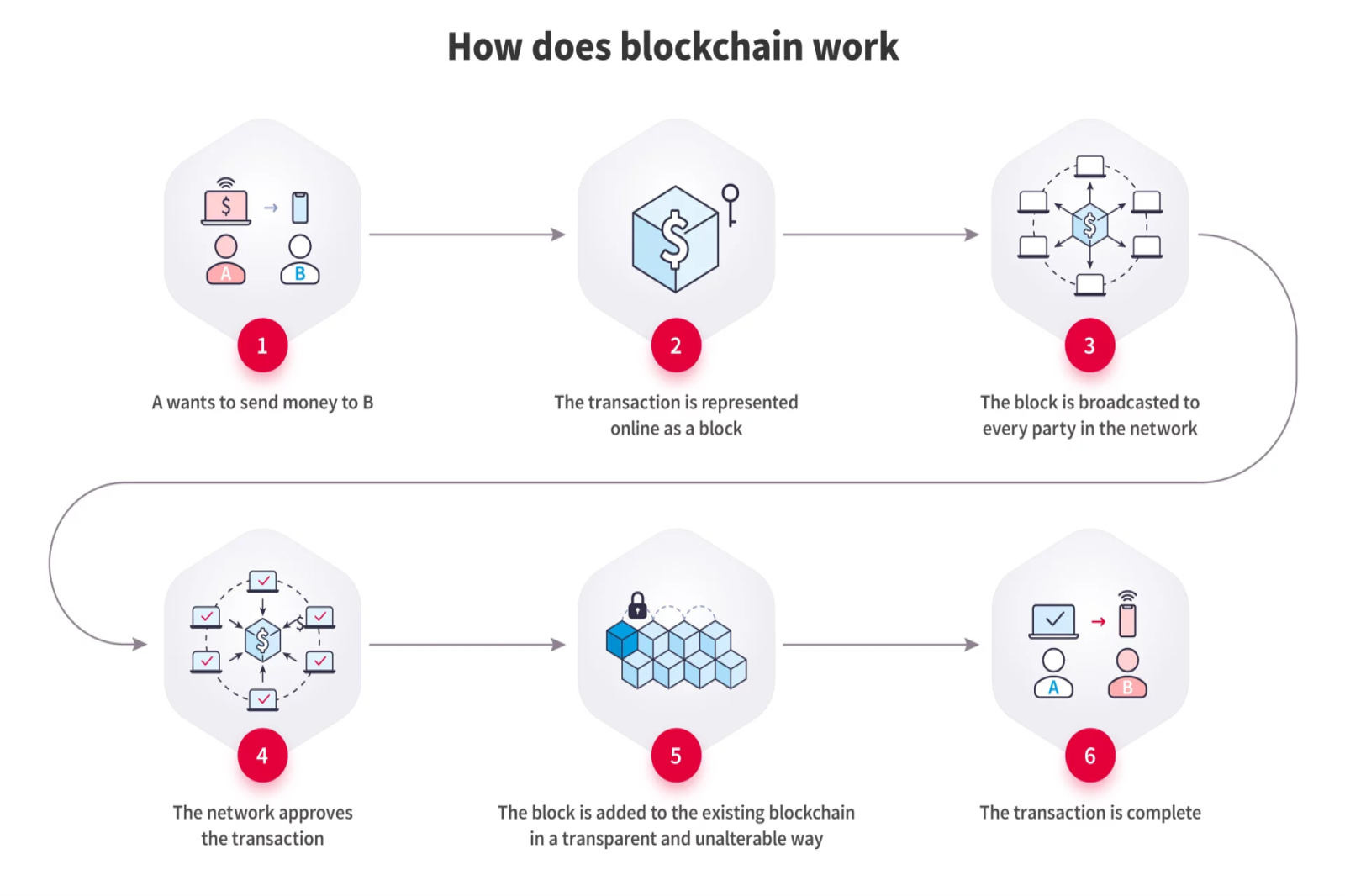

Table of Contents Introduction. 2 Definition and overview of blockchain technology. 2 Importance of blockchain in finance management. 2 Purpose of the presentation. 2 Understanding Blockchain. 2 Basics of blockchain technology. 2 Distributed ledger. 2 Decentralization. 3 Cryptography. 3 Key components of a blockchain. 3 Blocks. 3 Transactions. 3 Consensus mechanism.. 3 Different types of blockchains. 3 Public blockchains. 3 Private blockchains. 3 Consortium blockchains. 3 III. Implications of Blockchain in Finance Management. 3 Enhanced Security and Transparency. 3 Immutable records and tamper resistance. 3 Auditability and traceability. 3 Efficient and Cost-Effective Transactions. 4 Eliminating intermediaries. 4 Faster settlements and reduced transaction costs. 4 Smart Contracts and Automation. 4 Introduction to smart contracts. 4 Streamlined processes and reduced paperwork. 4 Fraud Prevention and Risk Mitigation. 4 Increased trust through consensus. 4 Improved identity verification and KYC processes. 4 Use Cases of Blockchain in Finance Management. 4 Cross-Border Payments and Remittances. 4 Supply Chain Finance. 4 Trade Finance and Letters of Credit. 4 Asset Tokenization and Securities Trading. 4 Peer-to-Peer Lending and Crowdfunding. 5 Insurance Claims and Underwriting. 5 Challenges and Considerations. 5 Scalability and performance issues. 5 Regulatory and legal concerns. 5 Interoperability between different blockchains. 5 Privacy and data protection. 5 Future Outlook. 5 Emerging trends and developments. 5 Collaboration between traditional finance and blockchain. 5 Potential impact on financial institutions and intermediaries. 5 VII. Conclusion. 5 Recap of key points. 5 Summary of blockchain's implications on finance management. 6 Potential benefits and opportunities. 6 Closing remarks. 6 I. Introduction A. Definition and overview of blockchain technology Blockchain technology is a decentralized and distributed ledger that records transactions across multiple computers. It enables secure and transparent transactions without the need for intermediaries. B. Importance of blockchain in finance management Blockchain has significant implications for finance management. It enhances security, reduces costs, automates processes, and mitigates fraud risks, transforming the way financial transactions are conducted. C. Purpose of the presentation The purpose of this presentation is to provide an understanding of blockchain technology and its implications in finance management. We will explore the key components of blockchain, its benefits, and various use cases in the financial industry. II. Understanding Blockchain A. Basics of blockchain technology 1. Distributed ledger Blockchain utilizes a distributed ledger, where multiple participants maintain and validate the transaction records collectively. This eliminates the need for a central authority and enhances trust. 2. Decentralization Blockchain operates in a decentralized manner, meaning no single entity has control over the entire network. This ensures transparency, resilience, and reduces the risk of a single point of failure. 3. Cryptography Blockchain uses cryptographic techniques to secure transactions and ensure data integrity. It employs cryptographic hash functions and digital signatures to authenticate and protect the information stored on the blockchain. B. Key components of a blockchain 1. Blocks Blocks are the building blocks of a blockchain and contain a set of transactions. Each block is linked to the previous block through a cryptographic hash, forming a chain of blocks. 2. Transactions Transactions represent the exchange of assets or information on the blockchain. They are recorded in blocks and are typically validated by network participants through a consensus mechanism. 3. Consensus mechanism Consensus mechanisms ensure agreement among network participants on the validity of transactions. It enables trust and prevents fraudulent activities. Common consensus mechanisms include Proof of Work (PoW), Proof of Stake (PoS), and Practical Byzantine Fault Tolerance (PBFT). C. Different types of blockchains 1. Public blockchains Public blockchains are open and accessible to anyone. They are maintained by a decentralized network of participants, and anyone can join the network, validate transactions, and create blocks. Bitcoin and Ethereum are examples of public blockchains. 2. Private blockchains Private blockchains are restricted to a specific group of participants. They provide privacy and control over the network, making them suitable for enterprises and organizations. Access to the blockchain is permissioned, and participants are often known entities. 3. Consortium blockchains Consortium blockchains are a hybrid between public and private blockchains. They are operated and maintained by a consortium or a group of organizations that have shared control over the network. Consortium blockchains offer a balance between openness and control. III. Implications of Blockchain in Finance Management A. Enhanced Security and Transparency 1. Immutable records and tamper resistance Blockchain's immutability ensures that once a transaction is recorded on the blockchain, it cannot be altered or deleted. This provides a high level of security and reduces the risk of fraud and tampering. 2. Auditability and traceability Blockchain's transparent nature enables easy auditing of transactions. Each transaction is recorded on the blockchain, creating an auditable trail of activities. This enhances transparency and accountability in financial transactions. B. Efficient and Cost-Effective Transactions 1. Eliminating intermediaries Blockchain eliminates the need for intermediaries, such as banks or clearinghouses, in financial transactions. This reduces costs, speeds up processes, and enables direct peer-to-peer transactions. 2. Faster settlements and reduced transaction costs Blockchain enables near-instantaneous settlements compared to traditional systems that may take days. It also reduces transaction costs by removing intermediaries and streamlining processes. C. Smart Contracts and Automation 1. Introduction to smart contracts Smart contracts are 2. Streamlined processes and reduced paperwork Smart contracts automate and streamline various financial processes, eliminating the need for manual paperwork and reducing human errors. This increases efficiency and accelerates transaction processing. D. Fraud Prevention and Risk Mitigation 1. Increased trust through consensus Blockchain's consensus mechanisms foster trust and prevent fraudulent activities. The distributed nature of blockchain ensures that transactions are verified by multiple participants, reducing the risk of fraud or manipulation. 2. Improved identity verification and KYC processes Blockchain technology can enhance identity verification and Know Your Customer (KYC) processes. It allows for secure storage and sharing of verified user data, reducing the risk of identity theft and fraud. IV. Use Cases of Blockchain in Finance Management A. Cross-Border Payments and Remittances Blockchain facilitates faster and cheaper cross-border payments by eliminating intermediaries, reducing fees, and providing real-time transaction tracking. B. Supply Chain Finance Blockchain enhances supply chain finance by enabling transparent and secure tracking of goods, verifying authenticity, reducing fraud, and streamlining payment processes. C. Trade Finance and Letters of Credit Blockchain simplifies trade finance by digitizing and automating the processing of letters of credit, reducing paperwork, and improving trust among participants. D. Asset Tokenization and Securities Trading Blockchain enables the tokenization of assets such as real estate or artwork, making them divisible and tradable. It enhances liquidity, simplifies ownership transfer, and reduces intermediaries in securities trading. E. Peer-to-Peer Lending and Crowdfunding Blockchain platforms facilitate peer-to-peer lending and crowdfunding by connecting borrowers directly with lenders, automating loan agreements, and providing transparency and auditability. F. Insurance Claims and Underwriting Blockchain streamlines insurance processes by automating claims processing, reducing fraud through transparent records, and improving underwriting accuracy through access to verified data. V. Challenges and Considerations A. Scalability and performance issues Blockchain faces challenges in scaling to accommodate a large number of transactions and maintaining performance. Solutions like layer-two protocols and sharding are being explored to address these challenges. B. Regulatory and legal concerns Blockchain's decentralized nature raises regulatory and legal concerns, such as data privacy, cross-border transactions, and compliance with existing financial regulations. Regulatory frameworks need to evolve to address these issues. C. Interoperability between different blockchains Interoperability between different blockchains is essential for seamless integration and exchange of assets and information. Efforts are underway to develop standards and protocols for interoperability. D. Privacy and data protection While blockchain provides transparency, preserving privacy and protecting sensitive data is crucial. Privacy-enhancing technologies like zero-knowledge proofs and secure multiparty computation are being developed to address these concerns. VI. Future Outlook A. Emerging trends and developments Emerging trends include the integration of blockchain with other technologies like artificial intelligence, Internet of Things, and decentralized finance (DeFi). These developments have the potential to revolutionize finance management further. B. Collaboration between traditional finance and blockchain Traditional financial institutions are exploring blockchain technology and collaborating with blockchain startups to leverage its benefits. Partnerships and consortia are being formed to drive innovation and adoption in the financial industry. C. Potential impact on financial institutions and intermediaries Blockchain has the potential to disrupt traditional financial institutions and intermediaries. They will need to adapt and innovate to remain competitive in a decentralized and digitally transformed financial landscape. VII. Conclusion A. Recap of key points Blockchain technology is a decentralized and transparent ledger that offers enhanced security, efficiency, automation, and fraud prevention in finance management. B. Summary of blockchain's implications on finance management Blockchain technology improves security, reduces costs, stream C. Potential benefits and opportunities Implementing blockchain in finance management can lead to reduced transaction costs, faster settlements, improved fraud prevention, and increased efficiency and transparency, unlocking new opportunities for innovation and growth. D. Closing remarks Blockchain technology has the potential to reshape the finance industry by revolutionizing how transactions are conducted, recorded, and verified. Embracing blockchain's capabilities can drive a more secure, efficient, and inclusive financial ecosystem.

by Youness El Kandoussi | 3 years ago | 0 Comment(s) | 1557 Share(s) | Tags :

POST COMMENT

COMMENTS(0)

No Comment yet. Be the first :)