Introduction

Dans le secteur bancaire, les risques sont omnipr sents et vari s. Parmi ces risques, le risque l gal occupe une place pr pond rante en tant que composante du risque op rationnel. Ce dernier inclut tout v nement r sultant de processus internes inad quats ou d faillants, de personnes, de systèmes ou d' v nements externes. Le paysage du risque l gal au sein des banques marocaines est en constante volution, influenc par divers facteurs tels que les r gulations nationales et internationales, les pratiques de gouvernance, ainsi que l'environnement conomique et social.

D finition et Cadre R glementaire

Le risque l gal se d finit comme le risque de pertes financières ou de r putation que peuvent encourir les banques en raison de poursuites judiciaires, de sanctions r glementaires ou de non-conformit aux lois et r glementations en vigueur. Au Maroc, ce cadre r glementaire est principalement dict par Bank Al-Maghrib, l'autorit de supervision bancaire, ainsi que par des normes internationales telles que celles dict es par le Comit de Bâle.

Les Sources du Risque L gal

Le risque l gal est omnipr sent dans le secteur bancaire et peut provenir de diverses sources. Comprendre ces sources est crucial pour laborer des strat gies efficaces de gestion et de mitigation. Voici un examen plus d taill des principales sources de risque l gal dans les banques marocaines :

1. La Non-conformit R glementaire

La non-conformit r glementaire survient lorsque les banques ne respectent pas les lois et r glementations en vigueur, qu'elles soient locales ou internationales. Cela peut inclure :

Non-respect des exigences de capital : Les banques doivent maintenir des niveaux sp cifiques de capital pour couvrir les risques. Ne pas se conformer à ces exigences peut entraîner des sanctions.

Non-respect des règles de lutte contre le blanchiment d'argent (LBA) : Les banques doivent mettre en place des mesures pour d tecter et pr venir le blanchiment d'argent. Une non-conformit peut conduire à des amendes s vères et à une perte de r putation.

Non-conformit aux r glementations fiscales : Les erreurs ou omissions dans le respect des obligations fiscales peuvent entraîner des poursuites judiciaires et des p nalit s financières.

2. Les Litiges Commerciaux

Les litiges commerciaux peuvent d couler de conflits avec diverses parties prenantes telles que les clients, les fournisseurs ou les partenaires commerciaux. Ces litiges peuvent inclure :

Les diff rends contractuels : D saccords sur l'ex cution ou l'interpr tation des contrats peuvent mener à des poursuites judiciaires.

Les r clamations des clients : Les clients peuvent intenter des actions en justice pour des pratiques perçues comme d loyales ou frauduleuses, telles que des frais cach s ou des conseils financiers inappropri s.

Les conflits avec les fournisseurs : Les litiges peuvent survenir concernant la qualit des services ou des produits fournis, ou encore le non-respect des d lais contractuels.

3. La Fraude et la Corruption

La fraude et la corruption repr sentent des risques significatifs pour les banques et peuvent se manifester de plusieurs façons :

Fraude interne : Des employ s peuvent commettre des actes frauduleux tels que le d tournement de fonds, la falsification de documents ou la manipulation des comptes.

Fraude externe : Les banques peuvent être victimes de fraudes perp tr es par des clients ou des tiers, incluant les fraudes à la carte de cr dit, les escroqueries par phishing, ou les cyberattaques.

Corruption : Les pratiques de corruption, telles que les pots-de-vin ou les conflits d'int rêts, peuvent entraîner des sanctions s vères et une perte de confiance de la part des parties prenantes.

4. Les Violations de la Confidentialit des Donn es

Avec la digitalisation croissante des services bancaires, les violations de la confidentialit des donn es sont devenues une source majeure de risque l gal :

Incidents de s curit : Les cyberattaques, telles que les piratages de donn es, peuvent compromettre des informations sensibles des clients, entraînant des poursuites judiciaires et des sanctions r glementaires.

Mauvaise gestion des donn es : La non-conformit aux lois sur la protection des donn es, comme le Règlement G n ral sur la Protection des Donn es (RGPD), peut entraîner des amendes importantes et des actions en justice.

Fuites d'informations : Les erreurs humaines ou les d faillances des systèmes peuvent conduire à la divulgation involontaire de donn es confidentielles, affectant la r putation de la banque et la confiance des clients.

Les D fis Sp cifiques aux Banques Marocaines

La gestion du risque l gal dans les banques marocaines est particulièrement complexe en raison de plusieurs d fis sp cifiques. Ces d fis sont li s à des facteurs internes et externes qui influencent les op rations quotidiennes des institutions bancaires. Voici une analyse d taill e des principaux d fis auxquels elles sont confront es :

1. L'Évolution Rapide des R gulations

Les r gulations bancaires au Maroc et à l'international voluent rapidement, n cessitant une capacit d'adaptation continue :

Modifications fr quentes des r gulations locales : Les autorit s de supervision, comme Bank Al-Maghrib, introduisent r gulièrement de nouvelles règles pour renforcer la stabilit financière et prot ger les consommateurs. Les banques doivent rester inform es de ces changements pour viter des sanctions pour non-conformit .

Adoption de r gulations internationales : Les r gulations internationales, telles que les accords de Bâle III, imposent des exigences strictes en matière de capital, de liquidit et de gestion des risques. Les banques marocaines doivent aligner leurs pratiques sur ces normes globales, ce qui peut n cessiter des ajustements op rationnels et financiers significatifs.

Complexit des mises en conformit : La mise en conformit avec les nouvelles r gulations peut être coûteuse et n cessiter des ressources sp cialis es. Cela inclut la formation des employ s, la mise à jour des systèmes informatiques et la r vision des politiques internes.

2. La Complexit des Affaires Transfrontalières

Les banques marocaines sont de plus en plus engag es dans des transactions internationales, ce qui ajoute une couche de complexit suppl mentaire à la gestion du risque l gal :

Multiples juridictions : Les transactions transfrontalières impliquent le respect des lois de plusieurs pays. Chaque juridiction a ses propres r gulations, exigences fiscales, et pratiques de gouvernance. Naviguer dans ce labyrinthe l gal n cessite une expertise juridique tendue et une coordination efficace.

Risques de non-conformit : Les diff rences entre les r gulations locales et trangères peuvent entraîner des risques de non-conformit . Par exemple, une transaction conforme aux r gulations marocaines pourrait violer les r gulations d'un autre pays.

Sanctions internationales : Les banques marocaines doivent galement se conformer aux sanctions internationales impos es par des organismes tels que l'ONU ou l'Union Europ enne. Le non-respect de ces sanctions peut entraîner des amendes lourdes et des restrictions op rationnelles.

3. La Digitalisation

L'adoption croissante des technologies financières (FinTech) et des services bancaires en ligne expose les banques à de nouveaux d fis en matière de risque l gal :

Cybers curit : Avec l'augmentation des cyberattaques, les banques doivent renforcer leurs systèmes de s curit pour prot ger les donn es sensibles des clients. Les violations de donn es peuvent entraîner des poursuites judiciaires et des sanctions r glementaires.

Protection des donn es : La gestion des donn es personnelles est soumise à des r gulations strictes, telles que le Règlement G n ral sur la Protection des Donn es (RGPD). Les banques doivent assurer la confidentialit et l'int grit des informations qu'elles d tiennent pour viter des amendes et des pertes de r putation.

Innovation rapide : Le d veloppement rapide de nouvelles technologies et de nouveaux produits financiers pose des d fis en termes de r gulation. Les banques doivent naviguer dans un environnement où les r gulations peuvent ne pas suivre le rythme des innovations technologiques, cr ant des zones grises en matière de conformit .

Strat gies de Gestion du Risque L gal

Pour att nuer le risque l gal, les banques marocaines adoptent plusieurs strat gies qui visent à renforcer leur conformit et à minimiser les risques associ s. Ces strat gies sont essentielles pour maintenir la stabilit financière et prot ger la r putation des institutions bancaires. Voici une analyse d taill e des principales strat gies de gestion du risque l gal :

1. La Mise en Place de Politiques de Conformit Robustes

Les politiques de conformit robustes sont la première ligne de d fense contre le risque l gal :

Élaboration de proc dures internes strictes : Les banques tablissent des proc dures d taill es pour chaque aspect de leurs op rations afin de garantir la conformit avec les r gulations locales et internationales. Cela inclut des processus pour la gestion des transactions, l'octroi de cr dits, et le traitement des r clamations des clients.

Mise à jour r gulière des politiques : Les r gulations voluent constamment, et les banques doivent adapter leurs politiques en cons quence. Cela implique une r vision r gulière des proc dures internes et des ajustements pour refl ter les nouvelles exigences r glementaires.

Culture de conformit : Les banques encouragent une culture d'entreprise où la conformit est int gr e dans les valeurs et les pratiques quotidiennes. Cela aide à pr venir les violations involontaires et à promouvoir des comportements thiques parmi les employ s.

2. La Formation Continue

La formation continue des employ s est cruciale pour maintenir un haut niveau de conformit :

Programmes de sensibilisation : Les banques organisent des sessions de sensibilisation pour informer les employ s des dernières r gulations et des bonnes pratiques en matière de conformit . Cela inclut des formations sur la lutte contre le blanchiment d'argent, la protection des donn es, et les normes de conduite professionnelle.

Formation sp cialis e : Les employ s des d partements cl s, tels que la conformit , les services juridiques, et les op rations, reçoivent des formations sp cialis es pour approfondir leurs connaissances et comp tences. Cela leur permet de g rer efficacement les aspects complexes de la r glementation bancaire.

Évaluations r gulières : Les banques valuent r gulièrement les connaissances et les comp tences des employ s en matière de conformit par le biais de tests et d' valuations. Cela permet d'identifier les lacunes et de fournir des formations suppl mentaires si n cessaire.

3. La Surveillance et l'Audit

La surveillance continue et les audits internes sont essentiels pour d tecter et corriger rapidement les anomalies :

Systèmes de contrôle interne : Les banques mettent en place des systèmes de contrôle interne pour surveiller les transactions et les op rations en temps r el. Ces systèmes aident à d tecter les comportements suspects et à pr venir les fraudes.

Audits r guliers : Les d partements d'audit interne effectuent des examens r guliers des op rations bancaires pour s'assurer de leur conformit avec les r gulations. Les audits permettent d'identifier les faiblesses et de recommander des am liorations.

Rapports de conformit : Les banques pr parent des rapports de conformit p riodiques pour les r gulateurs et les conseils d'administration. Ces rapports fournissent une vue d'ensemble de l' tat de la conformit et des mesures prises pour corriger les carts.

4. Le Recours à des Conseils Juridiques

La collaboration avec des experts juridiques est une strat gie cl pour anticiper et g rer les risques l gaux :

Conseillers juridiques internes et externes : Les banques emploient des conseillers juridiques internes et collaborent avec des cabinets d'avocats sp cialis s pour obtenir des avis sur les questions complexes de r glementation. Ces experts aident à interpr ter les lois et à d velopper des strat gies de conformit .

Veille juridique : Les conseillers juridiques effectuent une veille constante des volutions l gislatives et r glementaires. Cela permet aux banques d'anticiper les changements et de s'y pr parer en cons quence.

Gestion des litiges : En cas de litiges, les conseillers juridiques repr sentent les banques et les assistent dans les n gociations et les proc dures judiciaires. Leur expertise est essentielle pour minimiser les impacts financiers et r putationnels des contentieux.

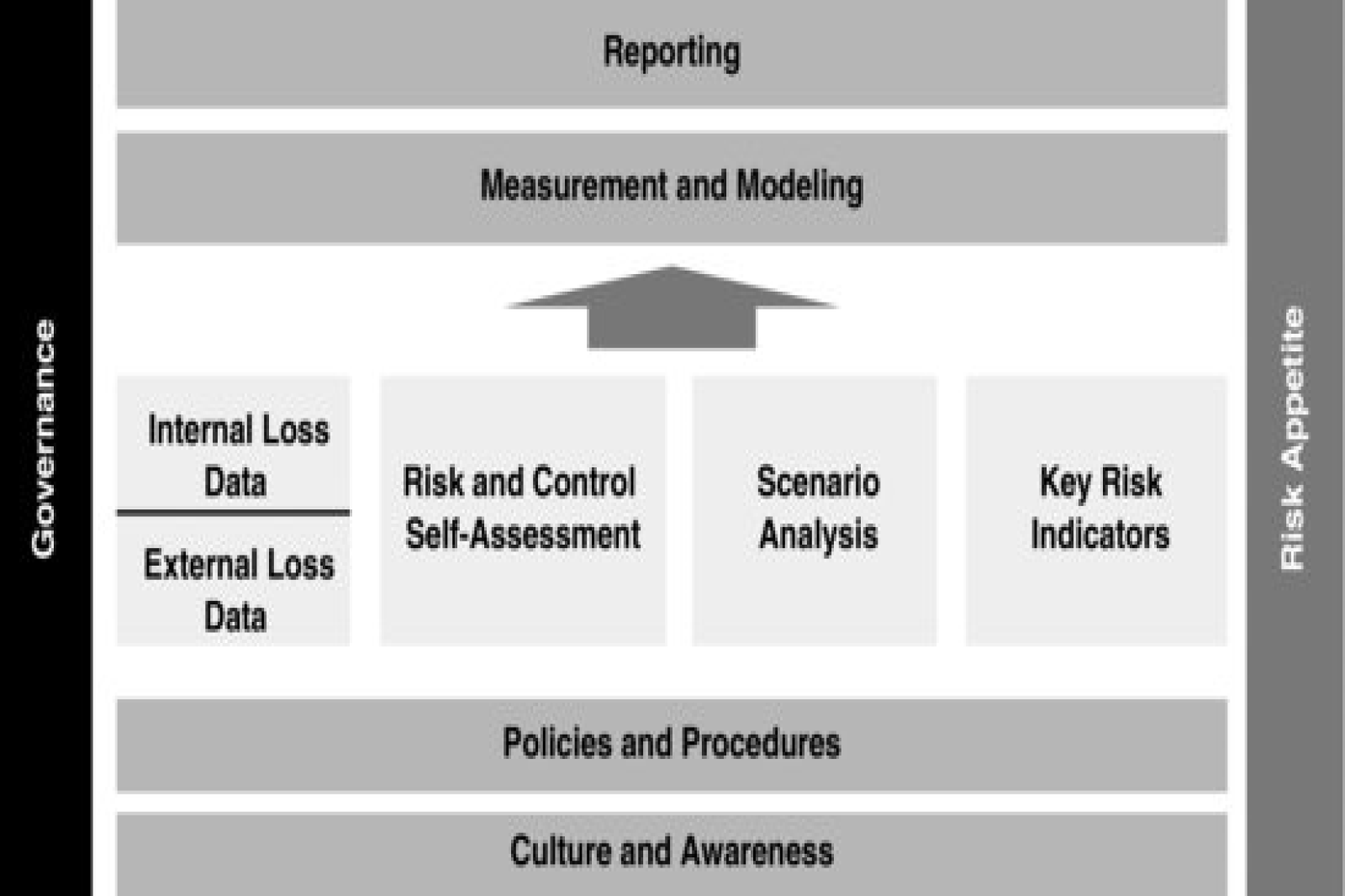

Conclusion G n rale

Le paysage du risque l gal, en tant que composante essentielle du risque op rationnel dans les banques marocaines, est marqu par des d fis croissants et vari s. L' volution rapide des r gulations, la complexit des affaires transfrontalières, et l'impact de la digitalisation exigent une vigilance constante et une capacit d'adaptation continue. Dans ce contexte, il est imp ratif pour les banques de d velopper et de maintenir un dispositif exhaustif de gestion du risque op rationnel.

La N cessit d'un Dispositif Exhaustif de Gestion du Risque Op rationnel

Un dispositif exhaustif de gestion du risque op rationnel doit int grer plusieurs l ments cl s pour être efficace :

Une Approche Holistique de la Conformit

Les banques doivent adopter une approche globale qui couvre tous les aspects de leurs op rations. Cela inclut non seulement la mise en place de politiques de conformit robustes mais aussi l'assurance que ces politiques sont comprises et mises en œuvre par tous les employ s.

Une culture d'entreprise ax e sur la conformit et l' thique est essentielle. Cela n cessite l'engagement de la direction et la sensibilisation de tous les niveaux de l'organisation.

Formation et Sensibilisation Continues

La formation continue des employ s est cruciale pour maintenir un haut niveau de conformit . Les programmes de formation doivent être r gulièrement mis à jour pour refl ter les changements r glementaires et les nouvelles menaces.

La sensibilisation aux risques l gaux et op rationnels doit être int gr e dans les programmes de d veloppement professionnel afin de garantir que tous les employ s sont conscients de leur rôle dans la gestion de ces risques.

Surveillance et Audit Rigoureux

La mise en place de systèmes de contrôle interne sophistiqu s et d’audits r guliers est indispensable pour d tecter et corriger rapidement les anomalies.

Les audits internes doivent être compl t s par des examens externes ind pendants pour assurer une valuation objective et complète des pratiques de gestion des risques.

Collaboration avec des Experts Juridiques et Techniques

La collaboration avec des conseillers juridiques et des experts en technologie est essentielle pour naviguer dans les complexit s des r gulations et des innovations technologiques.

Les banques doivent galement investir dans des technologies de pointe pour am liorer leurs capacit s de surveillance et de protection contre les cybermenaces.

Anticipation et Adaptation Proactives

Les banques doivent adopter une approche proactive pour anticiper les volutions r glementaires et les nouvelles tendances en matière de risque. Cela inclut la mise en place de processus de veille strat gique et l’analyse des sc narios futurs.

L'adaptabilit organisationnelle est galement cruciale. Les banques doivent être prêtes à r agir rapidement aux changements r glementaires et aux incidents op rationnels pour minimiser les impacts n gatifs.

POST COMMENT

COMMENTS(0)

No Comment yet. Be the first :)